Automotive Fuel Cell Market Research, 2033

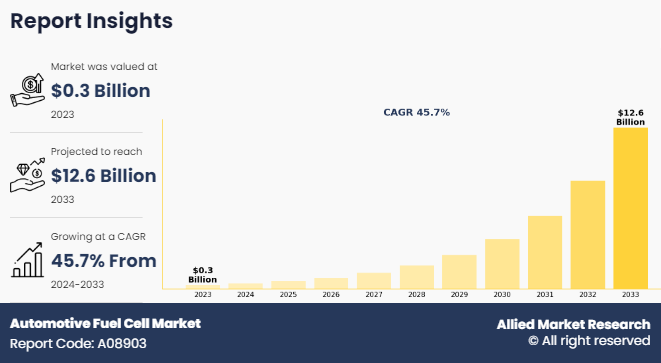

The global automotive fuel cell market size was valued at $0.3 billion in 2023, and is projected to reach $12.6 billion by 2033, growing at a CAGR of 45.7% from 2024 to 2033..

Key Takeaways

- On the basis of vehicle type, the passenger vehicles segment held the largest share in the automotive fuel cell in 2023.

- By Power Rating, the less than 150kW segment held the largest share in the market in 2023.

- On the basis of component, the fuel cell stack segment held the largest market share in 2023.

- On the basis of fuel cell type, the polymer electrolyte membrane fuel cells segment held the largest market share in 2023.

- On the basis of propulsion, the FCEV segment held the largest market share in 2023.

- On the basis of region, North America held the largest market share in 2023.

An automotive fuel cell is a device that converts chemical energy from hydrogen into electrical energy through an electrochemical process, powering electric vehicles (EVs). Unlike conventional internal combustion engines that burn fuel, fuel cells generate electricity by combining hydrogen with oxygen from the air, producing water vapor as the only byproduct. This technology offers high efficiency, zero emissions, and rapid refueling compared to traditional battery-powered EVs.

Automotive fuel cells are primarily used in vehicles such as passenger cars, buses, and trucks, with the potential to revolutionize the transportation sector by providing a sustainable alternative to fossil fuels. Their scalability and ability to reduce greenhouse gas emissions make them a promising solution for achieving long-term environmental goals in the automotive industry

The automotive fuel cell industry involves the development, production, and deployment of fuel cell technology in vehicles, aiming to offer a sustainable and efficient alternative to traditional internal combustion engines. Fuel cells generate electricity through an electrochemical reaction between hydrogen and oxygen, producing only water and heat as byproducts. This technology is increasingly adopted in various vehicle types, including passenger cars, buses, trucks, and material handling vehicles, due to its high efficiency, zero emissions, and potential to reduce dependence on fossil fuels.

For instance, in January 2024, Stellantis Pro One expanded its hydrogen fuel cell offerings to include mid-size and large vans, broadening its portfolio of eco-friendly commercial vehicles. This strategic move aims to cater to the growing demand for sustainable transportation solutions in the logistics and delivery sectors. By integrating hydrogen fuel cell technology into larger vehicle segments, Stellantis Pro One enhances the range, efficiency, and environmental performance of its vans, offering a viable alternative to traditional internal combustion engines. This expansion reflects Stellantis' commitment to innovation and sustainability, supporting the transition to zero-emission commercial fleets and contributing to the reduction of carbon footprints in urban and intercity transport.

For instance, in June 2024, Honda launched the new 2025 Honda CR-V e:FCEV at the Performance Manufacturing Center in Ohio, making it the first U.S.-made hydrogen fuel cell electric vehicle with plug-in EV charging capability and a 270-mile EPA driving range.

The rise in demand for zero-emission vehicles is significantly driving the automotive fuel cell market size, as consumers and governments increasingly seek alternatives to traditional internal combustion engines. Fuel cell electric vehicles (FCEVs) offer a compelling solution with their zero-emission operation, producing only water as a byproduct. This aligns with stringent environmental regulations and climate goals aimed at reducing greenhouse gas emissions and improving air quality.

As awareness of environmental issues rises and policies supporting clean transportation gain traction, the demand for FCEVs, supported by hydrogen fuel cells, is accelerating, driving market growth and encouraging further investments in hydrogen technology and infrastructure. Furthermore, expanding hydrogen refueling infrastructure, and surge in environmental regulations and emission standards have driven the demand for automotive fuel cell market share.

However, limited hydrogen refueling infrastructure is hampering the demand for the automotive fuel cell market forecast by restricting the practicality and convenience of hydrogen fuel cell electric vehicles (FCEVs). Without a widespread network of refueling stations, potential users are deterred by the inconvenience of locating refueling points and the uncertainty of fueling availability. This infrastructure gap limits the adoption of FCEVs, as drivers are hesitant to invest in vehicles with limited refueling options.

The slow development of hydrogen infrastructure further exacerbates this issue, creating a barrier to market growth and preventing broader acceptance and integration of hydrogen fuel cell technology in the automotive sector. Moreover, high cost of fuel cell technology, and limited consumer awareness and acceptance are major factors that hamper the growth of automotive fuel cell market share.

On the contrary, expansion into emerging markets with growing automotive sectors presents a lucrative opportunity for the automotive fuel cell industry. These regions, characterized by rapid economic growth and increasing urbanization, are experiencing rising vehicle ownership and environmental awareness. By introducing fuel cell technology in these markets, manufacturers can tap into new consumer bases eager for sustainable transportation solutions.

Emerging markets often benefit from supportive government policies aimed at reducing pollution and fostering green technologies. Capitalizing on these opportunities can drive substantial market growth, expand fuel cell infrastructure, and establish early dominance in in regions expected to witness significant dominance. By adopting this approach, companies can position themselves as leaders in the evolving market, ensuring long-term success and a competitive edge in the rapidly growing automotive sector.

Segment Review

The automotive fuel cell market is segmented into vehicle type, power rating, component, fuel cell type, propulsion, and region. On the basis of vehicle type, the market is divided into passenger vehicles, light commercial vehicles (LCVs), buses, trucks, and off-road vehicles. As per power rating, the market is segregated into less than 150 kW, 150 to 250 kW, and greater than 250 kW. On the basis of component, the market is segmented into fuel processor, power conditioner, fuel cell stack, air conditioner, air compressor, and humidifiers. By fuel cell type, the market is segmented into polymer electrolyte membrane fuel cell, direct methanol fuel cell, hydrogen, and ethanol. By propulsion, the market is bifurcated into FCEV and FCHEV. On the basis of region, it is analysed across North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa.

By Vehicle Type

On the basis of vehicle type, the passenger vehicles segment attained the highest market share in 2023 in the automotive fuel cell market due to rise in the adoption of hydrogen-powered cars, driven by increase in consumer demand for eco-friendly vehicles, government incentives, and advancements in fuel cell technology that enhance vehicle efficiency and range. Increase in government incentives, advancements in fuel cell technology, and the expanding hydrogen refuelling infrastructure contributed to the segment's dominance in the market.

Meanwhile, the off-road vehicles segment is projected to be the fastest-growing segment during the forecast period. This is due to their high energy demands and the benefits of fuel cells in providing extended range and quick refueling. The robust performance of fuel cells in challenging terrains and growing use in industries like mining and agriculture also contributed to this growth.

By Power Rating

On the basis of power rating, the less the 150kW segment attained the highest market share in 2023 in the automotive fuel cell due to its suitability for passenger vehicles, which dominate the market. These fuel cells offer an optimal balance of power, efficiency, and cost, making them ideal for smaller vehicles that prioritize range and fuel economy.

Meanwhile, the greater than 250kWsegment is projected to be the fastest-growing segment during the forecast period due to the rise in demand for high-power applications in commercial and heavy-duty vehicles. These fuel cells support larger and more demanding vehicles, such as buses and trucks, which require substantial power and longer ranges. Their advanced technology provides improved efficiency and performance, driving rapid growth in this segment for applications with significant energy needs.

By Component

On the basis of component, the fuel cell stack segment attained the highest market share in 2023 in the automotive fuel cell due to its critical role in converting hydrogen into electrical power. As the core component of fuel cell systems, fuel cell stacks are essential for performance and efficiency, making them pivotal in automotive applications. Their advancements in durability and efficiency directly influences the overall effectiveness and adoption of fuel cell vehicles.

Meanwhile, the humidifiers segment is projected to be the fastest-growing segment during the forecast period due to its critical role in maintaining optimal moisture levels within fuel cells for enhancing performance, efficiency, and longevity. The rise in demand for reliable fuel cell systems in vehicles drives the growth of the automotive fuel cell market. By regulating the humidity levels, humidifiers enhance the performance and longevity of fuel cell stacks, which are essential for efficient hydrogen conversion. As the demand for reliable and high-performance fuel cells grows, the need for advanced humidification solutions has accelerated, driving automotive fuel cell market growth.

By Region

On the basis of region, North America attained the highest market share in 2023 and emerged as the leading region in the automotive fuel cell market. This is due to a combination of factors, including substantial investments in research and development, favorable government policies, and a robust hydrogen infrastructure. The region benefits from significant support for clean energy technologies, with numerous incentives and subsidies aimed at promoting zero-emission vehicles. Major automotive manufacturers in North America are actively developing and deploying fuel cell vehicles, supported by a growing network of hydrogen refuelling stations.

However, Asia-Pacific is projected to be the fastest-growing region for the automotive fuel cell during the forecast period. This is due to a combination of supportive government policies, significant investments in hydrogen infrastructure, and rapid industrialization. Countries such as Japan, South Korea, and China are leading in fuel cell technology development and deployment, driven by aggressive climate goals and a strong focus on reducing urban air pollution. These nations are also investing heavily in expanding hydrogen refuelling networks and advancing fuel cell manufacturing capabilities.

The report analyzes the profiles of key players operating in the automotive fuel cell market such as Ballard Power Systems, Plug Power Inc., Hyundai Motor Company, Nuvera Fuel Cells, LLC, PowerCell Sweden AB, Horizon Fuel Cell Technologies Pte Ltd, Nedstack Fuel Cell Technology, ElringKlinger AG, Toyota Motor Corporation, and Intelligent Energy Limited. These players have adopted various strategies to increase their market penetration and strengthen their position in the automotive fuel cell market.

Competitive Analysis

The report analyzes the profiles of key players operating in the automotive fuel cell such as Ballard Power Systems, Plug Power Inc., Hyundai Motor Company, Nuvera Fuel Cells, LLC, PowerCell Sweden AB, Horizon Fuel Cell Technologies Pte Ltd, Nedstack Fuel Cell Technology, ElringKlinger AG, Toyota Motor Corporation, and Intelligent Energy Limited. These players have adopted various strategies to increase their market penetration and strengthen their position in the Automotive fuel cell market.

Rise in Demand for Zero-Emission Vehicles

The rise in demand for zero-emission vehicles is significantly boosting the automotive fuel cell market. As global concerns about climate change and air pollution intensify, governments and consumers are increasingly prioritizing environment-friendly transportation solutions. For instance, in September 2022, AVL launched a new hydrogen and fuel cell test center in Graz, marking a significant advancement in its commitment to hydrogen technology development.

This state-of-the-art facility is designed to enhance AVL’s capabilities in testing and optimizing hydrogen fuel cell systems, supporting the advancement of clean energy solutions. The center will focus on rigorous testing of fuel cell components and systems to improve performance, reliability, and efficiency. Fuel cell vehicles (FCVs), which emit only water vapor as a byproduct, align with this shift towards zero-emission mobility. Government policies, such as stricter emissions regulations and incentives for clean energy vehicles, are driving the adoption of fuel cells.

In addition, advancements in fuel cell technology, including improved efficiency, reduced costs, and expanding hydrogen refueling infrastructure, are making FCVs more viable and attractive. The automotive industry is responding to this demand by investing in research and development, resulting in a broader range of fuel cell vehicles, from passenger cars to commercial trucks. This growing interest and investment in zero-emission vehicles are propelling the fuel cell market. Therefore, rise in demand for for zero emission vehicles is driving the demand for the automotive fuel cell market.

Expanding Hydrogen Refuelling Infrastructure

Expanding hydrogen refueling infrastructure is significantly increasing the demand for the automotive fuel cell market by addressing one of the key barriers to widespread fuel cell vehicle (FCV) adoption—refueling convenience. As hydrogen refueling stations become more widespread, they reduce the range anxiety associated with fuel cell vehicles, making them a more practical choice for consumers. This expansion supports the growth of FCVs by providing the necessary refueling infrastructure to ensure that vehicles can be easily and quickly recharged.

For instance, in June 2024, Volkswagen launched next-generation hydrogen fuel cell technology with Kraftwerk Tubes, featuring a ceramic membrane for cost efficiency, and has filed a patent for a vehicle and hydrogen fuel cell stack with a 1,243-mile range, potentially marking its first fuel cell car.

In addition, the development of a robust hydrogen network signals a commitment to clean energy and fuels, encouraging both manufacturers and consumers to invest in fuel cell technology. As more refueling stations are built, it creates a positive feedback loop, where increased infrastructure drives higher FCV sales, which in turn justifies further investment in refueling facilities. This synergy between infrastructure development and vehicle adoption is accelerating the growth of the automotive fuel cell market. Therefore, expanding hydrogen refuelling infrastructure is driving the demand for the automotive fuel cell market.

Suge in Environment Regulation and Emission Standards

The surge in environmental regulations and emission standards is driving the demand for the automotive fuel cell market by creating a strong incentive for cleaner transportation solutions. Governments worldwide are implementing stricter emissions regulations to combat air pollution and climate change, requiring vehicles to produce lower or zero emissions.

For instance, in June 2024, Honda Motor launched the new CR-V e crossover SUV, which will be the first fuel cell passenger car produced in the U.S. by a carmaker. The CR-Ve will go on sale in the U.S. this year and be shipped to Japan by summer. It has a three-minute hydrogen filling time of 600 kilometers and a plug-in electric battery with a 60-kilometer range for short excursions.

Moreover, fuel cell vehicles (FCVs), which emit only water vapor, offer a compliant solution to these stringent standards. As regulatory frameworks tighten, automakers are increasingly investing in fuel cell technology to meet compliance requirements and avoid penalties. This regulatory pressure not only encourages manufacturers to develop and promote FCVs but also accelerates the adoption of fuel cell technology among consumers who are seeking environment-friendly options.

Furthermore, government incentives and subsidies for zero-emission vehicles further stimulate market growth, making fuel cell vehicles an attractive choice in the evolving regulatory landscape. Therefore, surge in environment regulation and emission standards is driving the growth of the automotive fuel cell market.

Limited Hydrogen Refueling Infrastructure

Limited hydrogen refuelling infrastructure is a significant barrier to the growth of the automotive fuel cell market. The availability of refuelling stations is critical for the widespread adoption of fuel cell vehicles (FCVs), as it directly impacts their practicality and convenience for consumers. With a sparse network of hydrogen stations, potential buyers are deterred by concerns about range anxiety and the difficulty of finding refuelling locations. This lack of infrastructure also discourages manufacturers from investing heavily in fuel cell technology due to uncertain returns on investment.

Furthermore, the slow development of hydrogen refuelling networks creates a catch-22 situation, where limited infrastructure hampers FCV adoption, and low adoption further discourages infrastructure expansion. To overcome this challenge, coordinated efforts between governments, industry stakeholders, and private investors are needed to build a more extensive and accessible hydrogen refuelling network, thereby facilitating the growth of the automotive fuel cell market. Therefore, limited hydrogen refuelling infrastructure is hampering the growth of the market.

High Cost of Fuell Cell Technology

The high cost of fuel cell technology is significantly hampering the demand for the automotive fuel cell market. Fuel cells, which are essential for converting hydrogen into electrical energy, involve expensive materials such as platinum catalysts and complex manufacturing processes. These costs contribute to higher vehicle prices, making fuel cell vehicles (FCVs) less affordable compared to conventional internal combustion engine vehicles and battery electric vehicles. This price disparity discourages consumers from purchasing FCVs, impacting overall market adoption.

In addition, the high cost of fuel cell technology limits economies of scale, as lower production volumes prevent cost reductions that could make FCVs more competitively priced. To overcome this barrier, ongoing research and development efforts are needed to find cost-effective alternatives to expensive materials and streamline manufacturing processes. Reducing the cost of fuel cell technology is crucial for making FCVs more accessible to consumers and stimulating market growth. Therefore, high cost of fuel cell technology is hampering the demand for the automotive fuel cell market.

Expansion into Emerging Market

The high cost of fuel cell technology is significantly hampering the demand for the automotive fuel cell market. Fuel cells, which are essential for converting hydrogen into electrical energy, involve expensive materials such as platinum catalysts and complex manufacturing processes. These costs contribute to higher vehicle prices, making fuel cell vehicles (FCVs) less affordable compared to conventional internal combustion engine vehicles and battery electric vehicles. This price disparity discourages consumers from purchasing FCVs, impacting overall market adoption.

In addition, the high cost of fuel cell technology limits economies of scale, as lower production volumes prevent cost reductions that could make FCVs more competitively priced. To overcome this barrier, ongoing research and development efforts are needed to find cost-effective alternatives to expensive materials and streamline manufacturing processes. Reducing the cost of fuel cell technology is crucial for making FCVs more accessible to consumers and stimulating market growth. Therefore, expansion into emerging market is driving the demand for the automotive fuel cell market opportunity.

Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the automotive fuel cell market analysis from 2023 to 2033 to identify the prevailing automotive fuel cell market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the automotive fuel cell market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global automotive fuel cell market trends, key players, market segments, application areas, and market growth strategies.

Automotive Fuel Cell Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 12.6 billion |

| Growth Rate | CAGR of 45.7% |

| Forecast period | 2023 - 2033 |

| Report Pages | 453 |

| By Vehicle Type |

|

| By Power Rating |

|

| By Component |

|

| By Fuel Cell Type |

|

| By Propulsion |

|

| By Region |

|

| Key Market Players | Nedstack Fuel Cell Technology, Intelligent Energy Limited, PLUG POWER INC., TW Horizon Fuel Cell Technologies, Hyundai Motor Company, NUVERA FUEL CELLS, LLC, TOYOTA MOTOR CORPORATION, PowerCell Sweden AB, Ballard Power Systems, ElringKlinger AG |

Upcoming trends in the global automotive fuel cell market include increased investments in hydrogen infrastructure, advancements in fuel cell efficiency and durability, growing adoption of fuel cell electric vehicles (FCEVs) in public transport and commercial applications, and collaborations between automakers and energy companies to promote hydrogen production and distribution.

The leading application of the automotive fuel cell market is in fuel cell electric vehicles (FCEVs), particularly in commercial transport sectors such as buses, trucks, and logistics vehicles, where long range and quick refueling are critical.

North America is the largest regional market for Automotive Fuel Cell.

$12.6 billion estimated industry size of Automotive Fuel Cell

Ballard Power Systems, Plug Power Inc., Hyundai Motor Company, Nuvera Fuel Cells, LLC, PowerCell Sweden AB, Horizon Fuel Cell Technologies Pte Ltd, Nedstack Fuel Cell Technology, ElringKlinger AG, Toyota Motor Corporation, and Intelligent Energy Limited.

Loading Table Of Content...

Loading Research Methodology...