Automotive Smart Antenna Market Research, 2033

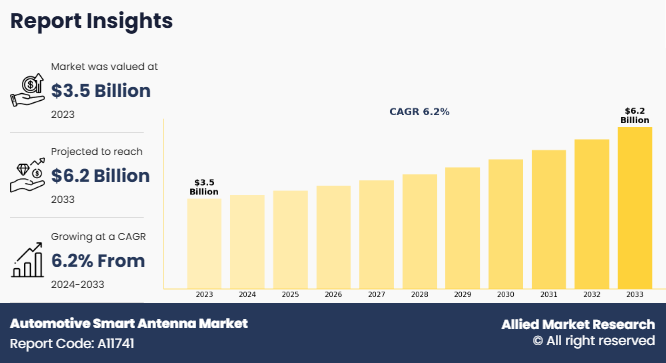

The global automotive smart antenna market size was valued at $3.5 billion in 2023, and is projected to reach $6.2 billion by 2033, growing at a CAGR of 6.2% from 2024 to 2033.

Automotive smart antennas are advanced antenna systems that are used in modern automobiles. Automotive smart antennas may include shark fin antennas, fixed mast antennas, blade antennas, patch antennas and others. Automotive smart antennas are used for various functions such as GPS, cellular connectivity, Wi-Fi and Bluetooth, AM/FM Radio, telematics and satellite radio applications. Smart antennas provide signal quality, reduce interference, and enhance overall communication reliability while integrating various sensors. Smart antennas enable better and more consistent communication for various in-car and external systems.

Report Key Highlighters:

- The automotive smart antenna industry study covers 14 countries. The research includes regional and segment analysis of each country in terms of value ($million) for the projected period 2024-2033.

- The study integrated high-quality data, professional opinions and analysis, and critical independent perspectives. The research approach is intended to provide a balanced view of global markets and to assist stakeholders in making educated decisions in order to achieve their most ambitious growth objectives.

- Over 3,700 product literature, annual reports, industry statements, and other comparable materials from major industry participants were reviewed to gain a better understanding of the market.

- The automotive smart antenna industry share is highly fragmented, into several players including

- Continental AG, TE Connectivity, Robert Bosch GmbH, Ficosa International S.A., Denso Corporation, Harman International, NXP Semiconductors, WISI Communications GmbH & Co. KG, TDK Corporation, and Harxon Corporation. The companies have adopted strategies such as product launches, contracts, expansions, agreements, and others to improve their market positioning.

Key Developments

The leading companies are adopting strategies such as acquisition, agreement, expansion, partnership, contracts, and product launches to strengthen their market position.

- On February 1, 2024 HARMAN International developed smart conformal antenna in collaboration with its parent company Samsung and Traffic Technology Services (TTS). The Smart Conformal Antenna is an advanced antenna system designed to integrate seamlessly into the shape of a vehicle, providing a sleek and aerodynamic design.

- On November 1, 2023 NXP Semiconductors launched next-generation single-chip Ultra-Wideband (UWB) solution, TrimensionTM NCJ29D6B to delivers secure and precise real-time localization improvements for secure car access. Trimension NCJ29D6A is the first monolithic UWB chip for automotive markets that combines secure localization and short-range radar with an integrated MCU. It allows OEMs to utilize one UWB system for multiple use cases ranging from child presence detection to secure car access.

- On July 1, 2022 Robert Bosch GmbH signed an agreement with Gapwaves, a Swedish tech company to develop and produce high-resolution radar antennas for automotive vehicle applications for highly automated driving. Gapwaves‐™ innovative antenna using waveguide technology enables cost efficient radar antennas with significantly increased performance.

The growth of the automotive smart antenna market growth is driven by growing advancement in autonomous driving and vehicle connectivity solutions, increasing use of cellular technology in connected vehicles, and technological advancement in the smart antenna. However, factors such as data security and privacy concerns for vehicles equipped with connected car features, and stringent standards for the automotive industry are anticipated to hinder the market growth rate during the forecast period. On the contrary, integration of 5G technology in smart antennas, and growing inclination towards hybrid and electric vehicle segment are expected to provide lucrative growth opportunities for market growth.

In recent years the demand for autonomous and self-driving vehicles has gained popularity owing to various benefits offered by these vehicles such as automatic parking, self-driving, autopilot, and other related safety features. Autonomous vehicles help in minimizing the need for human driver. Moreover, in recent years there has been increased investment by global companies such as Nvidia Corporation, Intel Corporation, Tesla, Inc., and others towards the development of autonomous vehicles.

For instance, on May 8, 2024, a London UK, UK-based startup, Wayve, announced they had received $1.5 billion in series C funding from leading chip manufacturing companies such as Microsoft and Nvidia Corporation. Wayve utilizes artificial intelligence, machine learning and robotics to develop autonomous vehicles and self-driving cars. The company is also among the first companies in the world to test and develop an end-to-end deep-learning autonomous driving system for public roads. Wayve is building foundation models for autonomous driving, which is similar to ChatGPT for driving; the system is capable of empowering any vehicle to see, think, and drive through different weather environments. According to the company, this investment will be used to support Wayve in developing and launching the first Embodied AI solutions for automobiles. The new systems will be used by the OEM to efficiently upgrade their car models to higher levels of driving automation, from L2-assisted driving to L4-automated driving.

Additionally on August 10, 2023, The California Public Utilities Commission (CPUC) announced the approval of legislation for additional operating authority to Cruise LLC and Waymo LLC to conduct commercial passenger service using driverless vehicles in San Francisco. The commissioner also stated both the companies to reduce the issues such as autonomous vehicles blocking the roads, causing traffic jams, and impeding emergency vehicles. If further such incidents are reported the California Public Utilities Commission (CPUC) could limit the companies number of vehicles on road or revoke their permit altogether.

The advancement in the autonomous and connected vehicles is creating more demand for advanced communication. As autonomous vehicle relies on sharing real time data with vehicles to vehicle (V2V), vehicle to infrastructure (V2I). To facilitate the demand for connectivity, OEMs are integrating their vehicles with advanced automotive smart antennas in order to ensure seamless connectivity, safety, and efficiency of modern vehicles. Thus, the growing demand for connectivity solutions is anticipated to drive the market for smart antennas during the forecast period.

However, modern automotive antennas utilize advanced systems and hardware which are integrated with multiple communication functions, such as GPS, Wi-Fi, Bluetooth, cellular, and vehicle-to-everything (V2X) technologies. This hardware is essential for connecting the vehicle with external networks, other vehicles, and infrastructure. As automotive smart antennas are a crucial aspect of the functioning of a vehicle, they need to meet stringent regulatory standards which are specifically designed to ensure the safety, environmental compliance, and reliability of vehicles. The automotive smart antennas need to align with the National Highway Traffic Safety Administration (NHTSA), European Automobile Manufacturers' Association (ACEA) and other regulatory associations, which increases the overall production cost of the product and increases its compliance challenges.

Segmental analysis

The automotive smart antenna market share is segmented on the basis of type, frequency, component, vehicle type, sales channel and region. On the basis of type the global market is analyzed into shark fin, fixed mast and others. Based on frequency, the market is segregated into high frequency, very high frequency, and ultra-high frequency. based on components, the global market is segregated into electronic control units, transceivers, power modules and others. On the basis of vehicle type, the global market is analyzed into passenger vehicles and commercial vehicles. Based on sales channel, the market is segregated into OEM and aftermarket. Region wise the market is segregated into North America, Europe, Asia-Pacific, Middle East and Africa and Latin America.

By Type

By type the, global automotive smart antenna market size has been segmented into shark fin, fixed mast and others. The shark fin segment accounted for the largest market share in 2023, owning to the growing use of telematics and smart connectivity features in automobiles. Modern shark fin antennas are equipped with various sensors which are used for transmitting signals related to satellites, radio signals and GPS. The demand for shark fin antennas is driven due to their sleek design which and aerodynamic capability which are highly in demand in modern automobiles.

By Frequency

On the basis of frequency, the global smart antenna market has been segregated into high frequency, very high frequency, and ultra high frequency. The very high frequency segment accounted for a the largest market share in 2023, owning to very high frequency antenna are ideal for communication systems, such as those used by emergency services in commercial fleets, and public safety vehicles. Very high frequency antennas are used in urban areas for medium-range communication. These frequency antennas are mostly deployed in entry-level vehicles and in majority of commercial fleets.

By Component

Based on components, the global smart antenna market has been analyzed into electronic control unit, transceivers, power modules and others. The electronic control unit segment accounted for the largest market share in 2023, owning to electronic control units are used to optimize performance for different communication tasks, such as GPS, radio, cellular, or Wi-Fi. The electronic control unit can manage multiple communication functions simultaneously, such as AM/FM radio, GPS, cellular, and Bluetooth; the growing production of vehicles with infotainment systems are anticipated to drive the market demand for electronic control units in antennas.

By Vehicle Type

On the basis of vehicle type the global market is segmented into Passenger Vehicle, and Commercial Vehicle. The passenger vehicle segment accounted for the largest market share in 2023, owning to the growing demand for the passenger vehicle segment due to the increasing demand for personal mobility solutions from developing economies. Moreover, there is a growing demand for advanced infotainment, navigation and infotainment technologies in the passenger vehicle segment, which is driving the demand for automotive smart antennas.

By Sales Channel

Based on sales channel the automotive smart antenna market has been analyzed into OEM and aftermarket. The OEM segment accounted for the largest market share in 2023, owning to the OEM automotive smart antenna parts usually come with a guarantee of quality and reliability as they meet the automotive manufacturer's original standards and specifications. Moreover, OEM parts are designed to meet the standards and specifications as the original parts, and OEM parts are guaranteed to fit and function as intended by the automobile manufacturer.

By Region

Region-wise, Asia-Pacific region held the largest market share in 2023, driven by several factors such as the region is witnessing an increase in migration of people from rural to urban areas, similarly, due to an increase in disposable income among people, the ownership of vehicles grew over the decade. Increase in the population growth in the cities lead to chaotic traffic jams and longer commute times. To address the issue, the government in the region is optimally utilizing vehicle and infrastructure date to improve transportation and make transportation more sustainable. The growing use of GPS and other connected vehicle technology is driving the demand for smart antennas in the region. Moreover, in recent years, India and other countries in Southeast Asia are witnessing a reduction in the price of internet connection and growth in mobile networks. Furthermore, the younger population in the region is willing to pay more for connected vehicle features, which further facilitates the automotive smart antenna market.

Integration of 5G Technology in Smart Antennas

As modern automobiles are becoming more connected with advanced technologies, they rely on the internet and other cellular technology. The growing demand for connected vehicle technologies creates lucrative opportunities for automotive smart antennas. According to an estimate by 2023, a quarter of all the global vehicle sold will be connected vehicle technologies such as enhanced navigation and smart access system. The demand for connected car is growing especially in the developing countries such as India, Mexico, Thailand and other south east Asian countries. For instance, in 2023 Kia Corporation sold 44% of its car with connected car features in India. Similarly, the company also stated that its connected car vehicle models are experiencing a growth rate of 30.9% CAGR which is faster as compared to 18% global CAGR.

According to the company, the Kia Seltos model contributes about 65% of the sales, and about 57% of all the customers purchasing Seltos opt for connected car features. The company is also developing popular features in vehicle which supports Hinglish commands, a combination of Hindi and English. Modern consumers are continuously demanding connected car feature such as 5G technology and hence with growing technological advancement the market for automotive smart antennas is expected to grow during the forecast period.

Technological Advancement in the Smart Antenna

The technological advancement in the smart antenna market is growing owing to increasing demand for connected vehicles and telematics. Smart antennas in modern vehicles are used to handle various functions related to V2X communication, GPS, Wi-Fi, Bluetooth and cellular networks. Likewise, smart antennas can operate in multiple frequency bands and support various communication standards, which help in reducing weight and the need for multiple antennas. The advancement in the smart antenna segment allows automobile manufacturers to develop advanced vehicle technologies such as connected vehicles, enhanced infotainment systems and integration with other vehicle systems. To tackle the growing demand for smart antenna components, manufacturers are increasing their focus on further development of smart antenna technology.

For instance, on January 9, 2023, KYOCERA AVX, a South Carolina-based manufacturer of electronic components, announced the launch of its A-Series low-profile, surface-mount automotive antennas. The new antenna series is used for applications such as wireless battery management systems, telematics control units, and vehicle access system. The antenna supports range of wireless technologies such as GNSS L1/L2/L5/L6, ISM, Wi-Fi 6E, Bluetooth, cellular, LTE, 5G, and UWB. Furthermore, the automotive antenna also supports a frequency range from 617MHz to 8.5GHz. According to the company new technology can deliver high frequency in smaller and compact design as compared to other antennas available in the market.

Key Benefits For Stakeholders

- This report provides a quantitative analysis automotive smart antenna market trends, segments, current trends, estimations, and dynamics of the automotive smart antenna market forecast and analysis from 2023 to 2033 to identify the prevailing automotive smart antenna opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global automotive smart antenna market analysis, market forecast, trends, key players, market segments, application areas, and market growth strategies.

Automotive Smart Antenna Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 6.2 billion |

| Growth Rate | CAGR of 6.2% |

| Forecast period | 2023 - 2033 |

| Report Pages | 280 |

| By Sales Channel |

|

| By Type |

|

| By Frequency |

|

| By Component |

|

| By Vehicle Type |

|

| By Region |

|

| Key Market Players | NXP Semiconductors, Continental AG, Harxon Corporation, TE Connectivity, DENSO CORPORATION, HARMAN International, Ficosa Internacional SA, WISI Communications GmbH & Co. KG, Robert Bosch GmbH, TDK Corporation |

Integration of lightweight materials for manufacturing of smart antennas are the upcoming market trend.

Passenger vehicle are the leading application of automotive smart antenna market.

Asia-Pacific is the largest regional market for automotive smart antenna market.

The global automotive smart antenna industry was valued at $3,475.60 million in 2023 and is projected to reach $6,236.2 million by 2033.

Continental AG, TE Connectivity, Robert Bosch GmbH, Ficosa International S.A., Denso Corporation, Harman International, NXP Semiconductors are some of the major companies operating in the market.

Loading Table Of Content...

Loading Research Methodology...