Commercial Helicopter Market Research, 2033

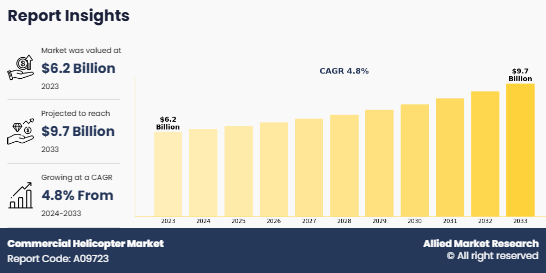

The global commercial helicopter market size was valued at $6.2 billion in 2023, and is projected to reach $9.7 billion by 2033, growing at a CAGR of 4.8% from 2024 to 2033.

Report Key Highlighters:

- The commercial helicopter market study covers 14 countries. The research includes regional and segment analysis of each country for the projected period 2024-2033.

- The study integrated high-quality data, professional opinions and analysis, and critical independent perspectives. The research approach is intended to provide a balanced view of global markets and to assist stakeholders in making educated decisions to achieve their most ambitious growth objectives.

- Over 3,700 product literature, annual reports, industry statements, and other comparable materials from major industry participants were reviewed to gain a better understanding of the market.

- The key players in the commercial helicopter industry are SpaceX, Blue Origin LLC, Airbus, Lockheed Martin Corporation, Northrop Grumman, Eutelsat, Viasat, Inc., SES S.A., Maxar Technologies, and Rocket Lab. These companies have adopted strategies such as product launches, contracts, expansions, agreements, and others to improve their market positioning.

A commercial helicopter is a rotorcraft used for civilian applications that involve passenger transport, cargo delivery, emergency services, and industrial operations. Unlike military helicopters, commercial helicopters are operated by private companies, government agencies, and service providers for various non-combat purposes.

These helicopters play a crucial role in industries such as emergency medical services (EMS), offshore oil and gas transport, corporate and VIP travel, law enforcement, aerial firefighting, and tourism. They range from light single engine helicopters used for training and private transport to heavy twin-engine helicopters designed for long-range operations and high-payload missions.

In addition, many commercial and government operations require twin-engine helicopters because they provide backup engine redundancy, ensuring safer operations over open water, mountainous terrain, and densely populated areas. Regulations in regions such as North America and Europe mandate the use of twin-engine helicopters for offshore oil and gas operations, medical evacuation (EMS), and corporate transport, further driving market demand.

Moreover, offshore energy companies are increasingly investing in twin-engine helicopters to ensure secure and efficient crew transfers to offshore platforms. Helicopters such as the Leonardo AW139, Airbus H175, and Sikorsky S92 are widely used in the oil and gas industry due to their long range, high payload capacity, and superior safety features. In addition, corporate aviation and VIP transport segments favor twin-engine models for enhanced comfort, noise reduction, and luxurious interiors, leading to increased sales in the business aviation sector.

Moreover, advancements in engine technology and lightweight materials are improving the performance and safety of single-engine helicopters. Manufacturers are introducing more fuel-efficient engines with lower emissions, making them more sustainable and attractive to operators looking to reduce costs. Helicopters such as the Robinson R44, Airbus H125, and Bell 505 are widely used in flight schools, private ownership, and tourism operations due to their affordability and ease of maintenance. Such new affordable models were introduced in the market to expand the commercial helicopter market share.

For instance, in March 2025, Robinson Helicopter expanded its lineup beyond light helicopters with the launch of the R88, a 10-seat, single-engine turbine helicopter featuring a clean-sheet design and a new type certificate. The first flight is expected this year, with certification and service entry planned later this decade. The company has already started accepting orders for the $3.3 million R88.

The R88 has a 275-cubic-foot cabin, capable of carrying up to eight passengers or 1,800 pounds of payload with full fuel. It is designed for aerial firefighting, air medical transport, utility work, and passenger transport, with a reconfigurable cabin to support multiple mission types.

The global commercial helicopter industry is expected to grow during the forecast period, driven by the rise in demand for air ambulances and EMS helicopters, expansion of offshore oil and gas operations fueling the need for heavy-lift helicopters, and growth in urban air mobility (UAM) and corporate travel boosting VIP helicopter sales. This positive outlook aligns with the commercial helicopter market forecast, highlighting sustained growth opportunities as operators adapt to evolving industry demands.However, high operating and maintenance costs and stringent aviation regulations and safety concerns are expected to hamper market commercial helicopter market growth during the forecast period.

Moreover, advancements in hybrid-electric propulsion and autonomous helicopters, along with increase in investments in aerial firefighting and disaster response helicopters, are expected to offer lucrative opportunities for the market in the future.

The commercial helicopter market is segmented into size, type, engine configuration, application, and region. On the basis of size, the market is divided into light helicopters, medium helicopters, and heavy helicopters. As per type, the market is segregated into piston helicopters and turbine helicopters. On the basis of engine configuration, the market is bifurcated into twin-engine helicopters and single-engine helicopters. By application, the market is categorized into oil & gas, transport, medical services, law enforcement & public safety, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Leading players and their key business strategies have been analyzed in the report to gain a competitive insight into the market. Key players covered in the report include SpaceX, Blue Origin LLC, Airbus, Lockheed Martin Corporation, Northrop Grumman, Eutelsat, Viasat, Inc., SES S.A., Maxar Technologies, and Rocket Lab.

Key Developments

The leading companies have adopted strategies such as acquisition, agreement, expansion, partnership, contracts, and product launches to strengthen their market position.

- In March 2025, Bell Textron Inc., a subsidiary of Textron Inc. and Omni Helicopters International Group (OHI, Omni), Latin America's leading air mobility solutions provider, announced a joint offshore operational evaluation program for the Bell 525 helicopter. The evaluation, set to take place over several months at Omnis high-tempo operation in Georgetown, Guyana, is pending type certification.

- In October 2024, Sikorsky, a Lockheed Martin company, established a Customer Advisory Group comprising leading commercial operators to guide the development and integration of next-generation vertical takeoff and landing (VTOL) technologies. The advisory group, which includes Bristow, Flexjet, Heli Offshore, Macquarie, Omni Helicopters International, Shell, and VIH Aviation Group, will collaborate with Sikorsky to define real-world operational requirements for future vertical lift systems. This partnership aims to accelerate advancements in Autonomy, Unmanned Aerial Systems (UAS), and Hybrid-Electric Propulsion, thus fostering innovation and driving industry growth.

- In March 2024, Enstrom Helicopter Corporation showcased its latest partnerships and new paint schemes at HAI HELI-EXPO 2024, a major helicopter trade show. Enstrom announced key company initiatives during a press conference at booth 6102 and unveiled new helicopter designs, highlighting its commitment to innovation in the industry.

Segmental analysis

The commercial helicopter market is segmented into size, type, engine configuration, application, and region. On the basis of size, the market is divided into light helicopters, medium helicopters, and heavy helicopters. As per type, the market is segregated into piston helicopters and turbine helicopters. On the basis of engine configuration, the market is bifurcated into twin-engine helicopters and single-engine helicopters. By application, the market is categorized into oil & gas, transport, medical services, law enforcement & public safety, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By size

By size, the commercial helicopter market is categorized into light helicopters, medium helicopters and heavy helicopters. The light helicopters segment accounted for the largest market share in 2023, due to their affordability, versatility, and ability to operate in various environments. These helicopters are widely used for private aviation, flight training, tourism, and law enforcement. One of the major market trends is the increasing adoption of light helicopters for urban air mobility (UAM) and short-distance transport services in congested cities.

By type

By type, the commercial helicopter market is categorized into piston helicopters and turbine helicopters. The turbine helicopters segment accounted for the largest market share in 2023, owing to their higher power output, improved reliability, and ability to operate in extreme conditions. These helicopters are extensively used in offshore transport, search and rescue (SAR), emergency medical services (EMS), and corporate travel. One of the major market trends is the increasing adoption of twin-engine turbine helicopters, which offer greater safety and range, making them preferred for long-distance operations.

By Engine Configuration

By engine configuration, the commercial helicopter market is categorized into twin engines and single engines. The single engine segment accounted for a dominant market share in 2023. These helicopters are preferred for short-distance travel, aerial surveys, and flight training due to their lower purchase and operational costs compared to twin-engine models. Many small and medium-sized businesses, as well as government agencies choose single-engine helicopters for cost-effective aerial operations in urban and rural environments.

By Application

By application, the commercial helicopter market is categorized into oil and gas, transport, medical services, law enforcement and public safety and others. The oil and gas segment accounted for a dominant market share in 2023, with a strong demand for medium and heavy-lift helicopters to transport personnel and equipment to offshore platforms. As oil companies expand deepwater drilling operations, the need for long-range, high-capacity helicopters such as the Sikorsky S-92, Airbus H225, H145 and Leonardo AW189 is increasing.

By Region

Region wise, North America held the largest commercial helicopter market share in 2023, driven by strong demand for emergency medical services (EMS), offshore oil and gas transport, corporate travel, and law enforcement applications. The region has a well-established helicopter infrastructure, with extensive networks of heliports, leasing companies, and operators providing diverse services. The U.S. and Canada collectively account for much of the helicopter fleet in the region, while Mexico is experiencing steady growth in offshore and private helicopter operations.

Rise in demand for air ambulances and EMS helicopters

The increasing demand for air ambulances and emergency medical services (EMS) helicopters is a significant driver of the commercial helicopter market. This growth is primarily due to the rising number of health emergencies, including accidents, cardiac arrests, strokes, and other critical conditions that require rapid medical intervention. Helicopters play a crucial role in transporting patients from remote or congested areas to hospitals with specialized care facilities. Their ability to bypass traffic and reach patients quickly has made them an essential component of modern healthcare systems.

Moreover, improvements in medical infrastructure have contributed to the expansion of air ambulance services. Many countries are investing in better-equipped hospitals, trauma centers, and helipads that allow helicopters to land directly at medical facilities. Governments and private healthcare providers are also expanding their emergency response networks by integrating helicopters into their medical evacuation plans.

In addition, the increasing availability of advanced medical equipment onboard helicopters has enhanced their capability to provide life-saving treatment during transport. Modern EMS helicopters are equipped with ventilators, defibrillators, and intensive care unit (ICU) setups, allowing paramedics to stabilize patients before reaching the hospital. This has led to a higher preference for helicopters over ground ambulances, especially in cases where time is critical.

Furthermore, many governments and non-profit organizations are actively supporting air ambulance services by offering subsidies, insurance coverage, and regulatory approvals for medical flights. The expansion of insurance policies that cover emergency air transport has also made EMS helicopters more accessible to patients in need. As healthcare awareness increases and more people seek faster and more efficient emergency care, the demand for air ambulance and EMS helicopters is expected to continue rising.

Expansion of offshore oil and gas operations driving demand for heavy-lift helicopters

The expansion of offshore oil and gas operations is driving the demand for heavy-lift helicopters in the commercial helicopter market. Offshore drilling and production sites are often located far from the mainland, requiring reliable and efficient transportation for personnel, equipment, and emergency evacuations. Helicopters play a crucial role in ensuring smooth operations by providing a safe and quick means of transport between offshore platforms and onshore facilities.

Moreover, as global energy demands continue to rise, oil and gas companies are expanding exploration and production activities into deeper and more remote waters. Regions such as the North Sea, the Gulf of Mexico, West Africa, and Southeast Asia have seen increased offshore activity, leading to greater reliance on helicopters for crew transfers and logistical support. Heavy-lift helicopters, which can carry larger payloads and operate in harsh weather conditions, are essential for these operations.

In addition, the need for improved safety and efficiency in offshore transport is further driving the adoption of modern heavy-lift helicopters. Oil companies are prioritizing helicopters with advanced navigation systems, better fuel efficiency, and higher passenger capacity to optimize crew rotations and reduce operational downtime. Helicopters such as the Sikorsky S-92 and the Airbus H225 are widely used due to their ability to fly long distances while ensuring passenger comfort and safety.

Furthermore, as older helicopter models are gradually being phased out, there is an increasing demand for newer, more fuel-efficient, and technologically advanced heavy-lift helicopters. Many oil and gas companies are investing in fleet upgrades to comply with evolving safety regulations and environmental standards. The continued expansion of offshore oil and gas operations, along with advancements in helicopter technology, is expected to sustain the demand for heavy-lift helicopters in the coming years.

High operating and maintenance costs

One of the major restraints in the commercial helicopter market is the high cost of operation and maintenance. Helicopters require frequent service, component replacements, and rigorous inspections to ensure their safety and performance. Unlike fixed-wing aircraft, helicopters have complex rotor systems and mechanical components that experience significant wear and tear, leading to higher maintenance costs. Operators must invest in specialized maintenance crews, spare parts, and regular overhauls, which significantly increase the overall expenses.

Moreover, fuel costs contribute to the high operational expenses of helicopters. Since helicopters have lower fuel efficiency compared to fixed-wing aircraft, operators must allocate a large budget for fuel consumption, especially for long-distance flights such as offshore transport and corporate travel. Rising fuel prices further adds to the financial burden, making helicopter operations expensive for both commercial and private users.

Advancements in hybrid-electric propulsion and autonomous helicopters

The development of hybrid-electric propulsion and autonomous helicopters is creating new opportunities in the commercial helicopter market. With the aviation industry focusing on reducing carbon emissions, helicopter manufacturers are investing in hybrid-electric and fully electric propulsion technologies to improve fuel efficiency and lower environmental impact. Hybrid-electric helicopters combine traditional turbine engines with electric power systems, allowing for reduced fuel consumption and quieter operations. This advancement is particularly beneficial for urban air mobility (UAM), where noise reduction is a key factor in gaining regulatory approval for city-wide helicopter services.

Moreover, autonomous helicopter technology is evolving rapidly, with companies such as Sikorsky and Airbus testing advanced flight control systems that reduce pilot workload and enhance operational safety. Autonomous or optionally piloted helicopters can be highly useful in applications such as cargo transport, emergency medical services, and military operations, where reducing human involvement can lower risks in hazardous environments. For instance, Sikorsky Matrix Technology is designed to enable autonomous flight capabilities in both new and existing helicopters, improving their operational flexibility.

Furthermore, the adoption of hybrid-electric and autonomous technology can reduce long-term operating costs, making helicopters more affordable for a wider range of commercial applications. As research and development in these areas continue to progress, hybrid-electric and autonomous helicopters are expected to revolutionize the market and create new business opportunities for operators and manufacturers.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the commercial helicopter market analysis from 2023 to 2033 to identify the prevailing commercial helicopter market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the commercial helicopter market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global commercial helicopter market trends, key players, market segments, application areas, and market growth strategies.

Commercial Helicopter Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 9.7 billion |

| Growth Rate | CAGR of 4.8% |

| Forecast period | 2023 - 2033 |

| Report Pages | 348 |

| By Size |

|

| By Type |

|

| By Engine Configuration |

|

| By Application |

|

| By Region |

|

| Key Market Players | Leonardo S.p.A., Airbus, Hindustan Aeronautics Ltd., Lockheed Martin Corporation, MD Helicopters Inc., Rostec, Robinson Helicopter Company, Inc., Bell Textron Inc., Enstrom Helicopter Corporation, Kaman Corporation. |

The upcoming trends of Commercial Helicopter Market in the globe are advancements in hybrid-electric propulsion and autonomous helicopters, along with increase in investments in aerial firefighting and disaster response helicopters

The leading application of Commercial Helicopter Market is oil and gas.

The largest regional market for Commercial Helicopter is North America

The global commercial helicopter market was valued at $6.2 billion in 2023, and is projected to reach $9.7 billion by 2033, growing at a CAGR of 4.8% from 2024 to 2033.

• The key players in the commercial helicopter market are SpaceX, Blue Origin LLC, Airbus, Lockheed Martin Corporation, Northrop Grumman, Eutelsat, Viasat, Inc., SES S.A., Maxar Technologies, and Rocket Lab.

Loading Table Of Content...

Loading Research Methodology...