Hepatitis C Testing Market Research, 2035

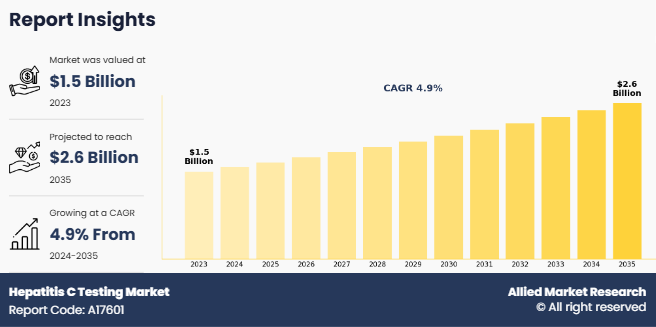

The global hepatitis C testing market size was valued at $1.5 billion in 2023, and is projected to reach $2.6 billion by 2035, growing at a CAGR of 4.9% from 2024 to 2035. The hepatitis C testing market is expanding, driven by rise in prevalence of hepatitis cases. According to the Wisconsin Department of Health Services, in 2023, 58% of all new hepatitis C virus (HCV) cases among females were in women of childbearing age (15-44 years). The estimated rate of mother-to-child transmission is approximately 6%, emphasizing the urgent need for preventive interventions. Currently, the only available preventive measure is treating HCV before pregnancy, highlighting the importance of early detection and timely treatment. Surge in incidence of hepatitis C, particularly in high-risk population, drives the need for enhanced diagnostic solutions and treatment accessibility.

Hepatitis C is a viral infection caused by the hepatitis C virus (HCV), primarily targeting the liver, and posing a significant risk of progressing to chronic liver disease, cirrhosis, and liver cancer if left untreated. The virus spreads primarily through blood-to-blood contact, commonly occurring due to the sharing of contaminated needles, unsterilized medical equipment, or blood transfusions performed before the widespread implementation of rigorous screening protocols. Given the severe health implications of hepatitis C, early and accurate diagnosis is critical in managing the disease effectively. The diagnostic process for hepatitis C typically begins with antibody tests, which help detect prior exposure to the virus. If the initial antibody test yields a positive result, confirmatory testing is performed using RNA-based assays to determine the presence and concentration of the virus in the bloodstream.

Key Takeaways

- On the basis of technique, the immunoassay segment dominated the market share in 2023. However, the PCR segment is anticipated to grow at the highest CAGR during the forecast period.

- On the basis of the test, the antibody test segment dominated the market share in 2023. However, the viral load test segment is anticipated to grow at the highest CAGR during the forecast period.

- On the basis of end user, the hospitals and diagnostic laboratory segment dominated the market share in 2023. However, the blood banks segment is anticipated to grow at the highest CAGR during the forecast period.

- By region, North America generated the largest revenue in 2023. However, Asia-Pacific is anticipated to grow at the highest CAGR during the forecast period.

Market Dynamics

The availability of standardized guidelines for hepatitis C testing plays a crucial role in driving market growth by ensuring consistent, evidence-based diagnostic practices and the widespread adoption of screening protocols. Leading health organizations, such as the Centers for Disease Control and Prevention (CDC) and the American Association for the Study of Liver Diseases (AASLD), in collaboration with the Infectious Diseases Society of America (IDSA), provide structured recommendations for HCV screening and diagnosis. The CDC emphasizes the use of FDA-approved laboratory-based tests, advocating for an initial HCV antibody screening followed by confirmatory HCV RNA testing to accurately detect active infections. These guidelines promote early detection, ensuring timely medical intervention and improved patient outcomes.

Global screening initiatives are further encouraged by these recommendations, targeting high-risk patients, pregnant women, and all adults to facilitate early disease management. The structured framework set by these guidelines enhances clinical decision-making and motivates governments, healthcare providers, and public health agencies to implement comprehensive testing programs aimed at reducing HCV transmission. The adoption of standardized protocols enhances the accessibility, accuracy, and reliability of testing methods, significantly increasing the demand for hepatitis C diagnostic kits across hospitals, diagnostic laboratories, and community healthcare settings. As more governments align with these recommendations and allocate resources for nationwide screening programs, the HCV diagnostic market continues to expand, supporting efforts for early detection and contributing to the global initiative to eliminate hepatitis C.

Rise in adoption of point-of-care (POC) testing is another major factor driving hepatitis C testing market growth, offering rapid, accurate, and accessible diagnostic solutions. Unlike traditional laboratory-based testing, POC diagnostics allow immediate on-site detection of HCV infections, significantly reducing turnaround times. This is particularly beneficial in resource-limited settings, rural areas, and emergency healthcare scenarios, where rapid results facilitate quicker clinical decisions and initial treatment initiation. Increase in demand for decentralized testing solutions boosts the development of advanced POC diagnostic kits that offer high sensitivity, specificity, and ease of use.

For example, Meril Life Sciences Pvt. Ltd. introduced TREDRO HCV Ab, a 3-dot rapid test device that utilizes flow-through technology to detect anti-HCV antibodies. This high-performance kit demonstrates over 99% sensitivity and more than 98% specificity across multiple HCV genotypes, ensuring reliable diagnostic accuracy. Designed with a user-friendly interface and inbuilt procedural controls, it enhances testing efficiency while accelerating HCV screening efforts. The availability of such highly accurate and accessible POC kits supports early diagnosis and facilitates market expansion as healthcare providers and governments increasingly integrate rapid testing into routine screening programs.

Despite these advancements, a significant barrier to market expansion remains the lack of awareness regarding hepatitis C. According to an article published on October 2023, by the National Library of Medicine, HCV affects an estimated 2.4 to 3 million individuals in the U.S. and approximately 58 million globally. Alarmingly, nearly half of those infected remain undiagnosed. A study involving 206 individuals with HCV found that only 60.1% were aware of their infection, suggesting that over 800,000 individuals in the U.S. alone remain undiagnosed.

The awareness gap is particularly pronounced among Mexican American and Asian population, limiting the effectiveness of widespread screening and diagnostic efforts. This low awareness level presents a challenge for hepatitis C testing kit manufacturers, as it directly impacts hepatitis C testing market growth. and the success of screening programs. Addressing this issue through targeted awareness campaigns and expanded education efforts is expected to be essential in advancing the market for HCV diagnostics and supporting global elimination goals.

Segmental Overview

The hepatitis C testing market size is segmented into technique, test, end user, and region. On the basis of technique, it is segregated into immunoassay, polymerase chain reaction (PCR), and others. The polymerase chain reaction (PCR) segment is further classified into real time PCR and other PCR. On the basis of test, it is classified into antibody test, genotype tests, and viral load test. On the basis of end user, it is categorized into hospital & diagnostic laboratory, blood banks, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

By Technique

The immunoassay segment dominated the hepatitis C testing market share in 2023. This was attributed to its cost-effectiveness, ease of use, and high-throughput capabilities. Its ability to rapidly screen for HCV antibodies makes it highly suitable for large-scale testing in hospitals, blood banks, and point-of-care settings, leading to widespread global adoption of hepatitis C testing.

However, the PCR test segment is expected to register the highest CAGR during the forecast period owing to its superior sensitivity, accuracy, and ability to detect low viral loads. Surge in adoption of real-time PCR assays for early and confirmatory diagnosis, along with advancements in automation and portable PCR platforms, fuels demand for hepatitis C testing solutions. In addition, increase in government initiatives for early screening programs and rise in need for high-throughput diagnostic solutions further drive the expansion of this segment.

By Test

The antibody test segment dominated the hepatitis C testing market share in 2023. This was attributed to its affordability, widespread availability, and ease of use for initial screening. Its extensive adoption across blood banks, hospitals, and diagnostic centers, along with government-led screening initiatives, contributed to its strong market presence. In addition, the quick turnaround time of antibody tests makes them a preferred option for large-scale testing programs.

However, the viral load test segment is expected to register the highest CAGR during the forecast period owing to its essential role in monitoring treatment response and disease progression. Increase in use of quantitative PCR-based assays, advancements in automated molecular diagnostics, and surge in focus on personalized treatment strategies are key growth drivers. Furthermore, rise in prevalence of hepatitis C cases and the expansion of government screening programs continue to fuel demand for viral load testing.

By End User

The hospital and diagnostic laboratory segment dominated the hepatitis C testing industry in 2023, primarily due to the high volume of tests conducted in these facilities, ensuring precise diagnosis and effective disease monitoring. The presence of advanced laboratory infrastructure, skilled healthcare professionals, and access to molecular testing technologies further fuel segment growth. In addition, government-led screening initiatives, increase in hospital visits, and rise in prevalence of hepatitis C infections contribute to its strong market position.

However, the blood banks segment is expected to register the highest CAGR during the forecast period driven by surge in need for safe blood transfusions and stringent screening protocols to prevent hepatitis C transmission. Increase in number of blood donation drives, advancements in nucleic acid testing (NAT), and government mandates for infectious disease screening further accelerate segment growth. Moreover, the expansion of blood banks in emerging economies supports the broader adoption of hepatitis C testing, strengthening market expansion.

By Region

Region wise, North America was the largest shareholder in the hepatitis C testing market in 2023 owing to the high prevalence of hepatitis C cases, well-developed healthcare infrastructure, and widespread use of molecular diagnostics. The region's market dominance was further supported by favorable government initiatives, strong reimbursement policies, and extensive awareness campaigns, which enhance early detection and diagnosis rates.

However, Asia-Pacific is anticipated to register the highest CAGR during the hepatitis C testing market forecast period owing to a significant hepatitis C burden, expanding healthcare infrastructure, and increase in government-led screening programs. Rise in awareness about HCV, improved access to advanced diagnostic technologies, and a large undiagnosed population contribute to market growth. Furthermore, the availability of cost-effective testing solutions and increase in healthcare investments further accelerate the adoption of hepatitis C testing across the region.

Competition Analysis

Competitive analysis and profiles of the major players in the hepatitis C testing market are Abbott Laboratories, Cosara Diagnostics Pvt Ltd, Meril Life Sciences Pvt. Ltd., Molbio Diagnostics Pvt. Ltd., Qiagen N.V., Trivitron Healthcare, Bio-Rad Laboratories, Inc., F.Hoffmann-La Roche Ltd., Hologic, Inc., and Thermo Fisher Scientific Inc. The key players have adopted product approval, partnership, and product launch as the key strategies for expansion of their product portfolio.

Recent Developments in Hepatitis C Testing Industry

- In September 2024, QIAGEN N.V. announced the expansion of its strategic partnership with Bio Manguinhos/Fiocruz. The partnership, initiated in 2009, supported Bio-Manguinhos/Fiocruz with reagents and instruments for testing samples for HIV and hepatitis C virus. With the expansion of this collaboration, Bio-Manguinhos is able to launch an advanced PCR-based molecular screening platform to detect malaria alongside HIV and hepatitis B & C virus (HCV and HBV), a capability previously unavailable in Brazil̢۪s blood donation program.

- In July 2023, F. Hoffmann-La Roche Ltd., India announced the launch of the Elecsys HCV Duo, which is India's first commercially available fully automated immunoassay that allows simultaneous and independent determination of the hepatitis C virus (HCV) antigen and antibody status from a single human plasma or serum sample. This means that the test is used to detect the early stage of infection, as well as when the patient is recovering from the virus, or even during chronic infection.

Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the hepatitis C testing market analysis from 2023 to 2035 to identify the prevailing hepatitis C testing market opportunity.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the hepatitis c testing market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global hepatitis c testing market trends, key players, market segments, application areas, and market growth strategies

Hepatitis C Testing Market Report Highlights

| Aspects | Details |

| Market Size By 2035 | USD 2.6 billion |

| Growth Rate | CAGR of 4.9% |

| Forecast period | 2023 - 2035 |

| Report Pages | 312 |

| By Technique |

|

| By Test |

|

| By End User |

|

| By Region |

|

| Key Market Players | Trivitron Healthcare, Cosara Diagnostics Pvt Ltd, Bio-Rad Laboratories, Inc. , Abbott Laboratories, Meril Life Sciences Pvt. Ltd., Qiagen N.V., Molbio Diagnostics Pvt. Ltd., Hologic, Inc., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd. |

Analyst Review

This section presents insights into the hepatitis C testing devices market. The market growth is primarily driven by the prevalence of hepatitis C infections, increase in number of awareness initiatives, and advancements in diagnostic technologies. They emphasized that innovations in molecular diagnostics, such as rapid point-of-care testing and multiplex assay kits, significantly enhance early detection and treatment accessibility. Surge in focus on decentralizing testing to reach high-risk population, particularly through mobile healthcare units and community-based programs, further propels market expansion.

In addition, importance of regulatory approvals and strategic collaborations in shaping market growth. The introduction of advanced diagnostic solutions that enable faster and more accurate detection drives adoption of hepatitis C testing solutions across healthcare settings. In addition, partnerships among healthcare providers, diagnostic companies, and government organizations play a crucial role in expanding access to hepatitis C testing. However, the challenges related to regulatory compliance and the need for skilled professionals to operate sophisticated diagnostic devices are identified as potential barriers to market growth.

North America dominated the market in 2023, due to its well-established healthcare infrastructure, rapid adoption of cutting-edge diagnostic technologies, and strong investment in research & development. The Asia-Pacific region is expected to experience the highest growth rate in the coming years driven by increase in government initiatives to improve hepatitis C screening, rise in healthcare expenditure, and surge in emphasis on early disease detection. The expansion of point-of-care testing facilities and improvements in healthcare accessibility are expected to further drive demand for hepatitis C testing solutions in emerging markets.

The total market value of hepatitis C testing market was $1.5 billion in 2023.

The market value of hepatitis C testing market is projected to reach $2.6 billion by 2035.

The forecast period for hepatitis C testing market is 2024 to 2035.

North America lead the market share in 2023 due to high awareness, healthcare access, and government initiatives, while Asia-Pacific is growing rapidly.

The base year is 2023 in hepatitis C testing market.

Advancements in diagnostic technologies, increasing prevalence of hepatitis C infections, and government screening initiatives drive market growth.

Hepatitis C testing detects the presence of the hepatitis C virus (HCV) in the blood. It includes antibody tests to check for past or present infection and nucleic acid tests (NATs) to confirm active infection. These tests help in early diagnosis, guiding treatment, and preventing liver complications.

Loading Table Of Content...

Loading Research Methodology...