Low Carbon Building Market Research, 2033

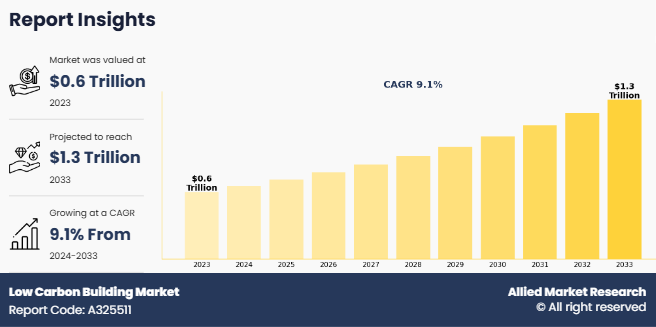

The global low carbon building market size was valued at $0.6 trillion in 2023, and is projected to reach $1.3 trillion by 2033, growing at a CAGR of 9.1% from 2024 to 2033.

Key Takeaways

- The global low carbon building market is highly fragmented, with several players including Honeywell International Inc., Johnson Controls, Saint-Gobain, Kingspan Group PLC, CEMEX S.A.B DE C.V., Skanska AB, CRH plc, VEXO International, Kenoteq, and VINCI Energies Building Solutions.

- More than 4,765 product literatures, industry releases, annual reports, and other such documents of major industry participants along with authentic industry journals, trade associations' releases, and government websites have been reviewed for generating high-value industry insights.

- The study integrated high-quality data, expert opinions and analysis, and crucial independent perspectives. This research approach aims to provide a balanced view of global markets and low carbon building market overview, assisting stakeholders in making informed decisions to achieve their most ambitious growth objectives.

- Low carbon building market news and key industry trends are also included in the report.

Introduction

A low carbon building is designed, constructed, and operated with the goal of minimizing its carbon footprint throughout its lifecycle. This involves reducing greenhouse gas emissions by using sustainable materials, incorporating energy-efficient technologies, and optimizing operational performance. Low carbon buildings often feature renewable energy sources, high-performance insulation, energy-efficient lighting and appliances, and innovative design techniques to reduce energy consumption.

The primary use of low carbon buildings is to combat climate change by minimizing environmental impact. They contribute to energy efficiency, lower utility costs, and improved indoor air quality. These buildings are commonly used in residential, commercial, and industrial sectors to promote sustainability. Additionally, they support green certification goals, such as LEED or BREEAM, and are vital in achieving global net-zero carbon emission targets.

Market Dynamics

The low carbon building market growth is driven by increasing awareness of climate change, stringent government regulations on carbon emissions, and rising demand for sustainable construction practices. Advancements in green building materials and technologies, coupled with incentives such as tax benefits and subsidies, further encourage the adoption of low carbon buildings. Moreover, the growing emphasis on energy efficiency and the global push towards net-zero targets are significant drivers for this sector.

Climate Change Mitigation is a key driver of low carbon buildings, as it focuses on reducing greenhouse gas (GHG) emissions to combat global warming. Buildings contribute significantly to GHG emissions, both during construction and operation. The construction process, from the extraction of raw materials to the transportation and processing of building components, emits a substantial amount of COâ‚‚. Additionally, during operation, buildings consume large amounts of energy for heating, cooling, lighting, and appliances, often relying on fossil fuels that emit carbon when burned. Mitigating climate change by reducing emissions from the built environment is therefore a critical step in achieving global climate goals.

To address this, low carbon buildings are designed to minimize their environmental impact. This includes enhancing energy efficiency, such as using high-performance insulation, energy-efficient windows, and efficient heating and cooling systems. By reducing energy consumption, low carbon buildings decrease the need for electricity produced by carbon-intensive sources like coal and natural gas, thereby cutting emissions. Moreover, integrating renewable energy systems such as solar panels or wind turbines into buildings can help reduce reliance on fossil fuels by allowing buildings to generate their own clean energy. These measures not only reduce a building’s carbon footprint but also contribute to broader national and global efforts to meet climate targets, such as those outlined in the Paris Agreement.

The emphasis on climate change mitigation is also driving innovation in construction materials. Using sustainable materials such as recycled steel, low-carbon concrete, and timber from responsibly managed forests reduces the embodied carbon of a building. These strategies collectively contribute to a lower overall carbon footprint for buildings, making them a crucial part of the solution to mitigating climate change and reducing global warming. However, the market faces restraints such as high initial costs of sustainable materials and technologies, limited availability of skilled labor, and challenges in retrofitting existing buildings to meet low carbon standards. These barriers can slow the adoption rate, particularly in developing regions.

On the other hand, the market presents immense opportunities, including the development of innovative low-carbon technologies, expansion into emerging markets, and increasing investments in green infrastructure. Growing urbanization and the rise of smart city projects worldwide offer a fertile ground for scaling low carbon building practices, making them a cornerstone of future construction trends.

Segments Overview

The low carbon building industry is segmented into building type, component, and region. Based on building type, the market is categorized into residential, commercial, and industrial. By component, the low carbon building market is classified into HVAC systems, green roofing & solar panels, lightning solution, and others. Region wise, the low carbon building market share is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Asia-Pacific was the highest revenue contributor, growing at a CAGR of 9.5%. The Asia-Pacific low carbon building market is experiencing rapid growth, driven by increasing urbanization, government initiatives, and rising awareness of sustainability and energy efficiency. As one of the most urbanized regions in the world, Asia-Pacific is undergoing a massive construction boom, with countries like China, India, Japan, South Korea, and Australia leading the charge toward low carbon construction. The region’s growing population and expanding urban areas present a unique opportunity to implement sustainable building practices that reduce carbon emissions.

Governments in the region are introducing stricter building codes and green building certifications to promote sustainable architecture. China, for instance, is implementing national energy efficiency standards and promoting green building certifications such as GB/T 50378. India’s Energy Conservation Building Code (ECBC) also encourages energy-efficient design in buildings. In addition, countries like Japan and Australia have adopted ambitious net-zero emissions targets, prompting a shift toward low carbon building practices. Japan's commitment to reducing energy consumption and carbon emissions is reflected in its energy-efficient design standards and emphasis on renewable energy integration.

Commercial segment was the highest revenue contributor to the market growing with a CAGR of 9.2%. The growth of low-carbon commercial buildings is driven by stringent government regulations promoting sustainability, corporate commitments to net-zero targets, and increasing investor focus on ESG (Environmental, Social, and Governance) criteria. Additionally, rising energy costs and the financial benefits of energy efficiency encourage businesses to adopt low-carbon solutions. Technological advancements, such as smart building automation and energy management systems, further support the transition by optimizing resource consumption. Consumer demand for environmentally responsible businesses, green certifications like LEED and BREEAM, and the availability of green financing options, including sustainability-linked loans, also play a crucial role in accelerating adoption. As urbanization and commercial real estate expansion continue, businesses and developers are prioritizing low-carbon buildings to enhance operational efficiency, reduce costs, and meet sustainability goals, driving significant market growth in this sector.

HVAC systems segment was the highest revenue contributor to the market growing with a CAGR of 8.9%. The growing demand for low-carbon building HVAC systems is driven by a combination of environmental regulations, sustainability goals, and advancements in energy-efficient technology. As buildings aim to reduce their carbon footprints, HVAC systems designed to optimize energy use and minimize greenhouse gas emissions are becoming increasingly popular. Key drivers include government incentives for green construction, rising energy costs, and the need for buildings to meet stricter energy efficiency codes. Innovations such as smart thermostats, energy recovery ventilation, and the integration of renewable energy sources (e.g., solar and geothermal systems) are enhancing the efficiency of HVAC systems. Additionally, the focus on indoor air quality and occupant comfort is pushing demand for HVAC solutions that not only conserve energy but also contribute to healthier living and working environments.

Competitive Analysis

The key players operating in the low carbon building market forecast are Honeywell International Inc., Johnson Controls, Saint-Gobain, Kingspan Group PLC, CEMEX S.A.B DE C.V., Skanska AB, CRH plc, VEXO International, Kenoteq, and VINCI Energies Building Solutions. Other players operating in the market include Holcim, TITAN Group, GreenJams, and others.

In Feb 2025, TITAN Group entered the South Asian market through a joint venture in India focused on low-carbon building materials. The venture, formed in collaboration with JAYCEE, a prominent Indian player in supplementary cementitious materials (SCMs), operated under the newly established entity Atlas EcoSolutions Private Limited, with TITAN Group holding a majority stake. This initiative enhanced TITAN’s geographical footprint and aligned with its strategic priority to expand its green product portfolio toward net zero.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the low carbon building market analysis from 2023 to 2033 to identify the prevailing low carbon building market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the low carbon building market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global low carbon building market trend, key players, market segments, application areas, and market growth strategies.

Low Carbon Building Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 1318.4 billion |

| Growth Rate | CAGR of 9.1% |

| Forecast period | 2023 - 2033 |

| Report Pages | 272 |

| By Building Type |

|

| By Component |

|

| By Region |

|

| Key Market Players | VEXO International, Saint-Gobain, Kenoteq, CEMEX S.A.B DE C.V., Kingspan Group PLC., Honeywell International Inc., VINCI Energies Building Solutions, CRH plc, Skanska AB, Johnson Controls |

Analyst Review

According to the opinions of various CXOs of leading companies, the low carbon building market is expected to witness an increase in demand during the forecast period. The key drivers of low carbon buildings include the global push to combat climate change by reducing greenhouse gas emissions and achieving net-zero targets. Stricter government regulations, such as energy efficiency mandates and carbon reduction policies, are accelerating adoption.

The low carbon building market offers numerous opportunities driven by technological advancements, global sustainability goals, and increasing urbanization. Innovations in green technologies, such as smart energy management systems, energy-efficient building materials, and renewable energy solutions like solar panels and geothermal heating, are creating new possibilities for reducing carbon footprints while enhancing building performance. These technologies are becoming more cost-effective, making them accessible to a broader market.

The rise of smart city projects globally provides a significant platform for integrating low carbon buildings into urban infrastructure. These projects emphasize energy efficiency, waste reduction, and sustainability, offering opportunities for developers to incorporate advanced low-carbon solutions from the planning stages. Emerging economies, experiencing rapid urbanization, present another key growth area as they adopt sustainable construction practices to meet rising demands for housing and infrastructure while aligning with global sustainability goals.

Additionally, the push for net-zero carbon emissions by governments and corporations has spurred investments in low carbon building projects. Financial incentives, such as tax credits, green bonds, and subsidies, further encourage adoption, creating a favorable business environment. Beyond environmental benefits, low carbon buildings offer cost savings in the form of reduced energy consumption, which appeals to both residential and commercial consumers.

Asia-Pacific is the largest regional market for Low Carbon Building.

The key players operating in the low carbon building market are Honeywell International Inc., Johnson Controls, Saint-Gobain, Kingspan Group PLC, CEMEX S.A.B DE C.V., Skanska AB, CRH plc, VEXO International, Kenoteq, and VINCI Energies Building Solutions.

By component, the HVAC systems segment was the highest revenue contributor to the market in 2023.

The low carbon building market size was valued at $0.6 trillion in 2023, and is estimated to reach $1.3 trillion by 2033, growing at a CAGR of 9.1% from 2024 to 2033.

The adoption of low carbon buildings is driven by the urgent need to mitigate climate change, stricter government policies on carbon emissions, and growing awareness of sustainable practices.

Loading Table Of Content...

Loading Research Methodology...