Medical Devices Market Research, 2033

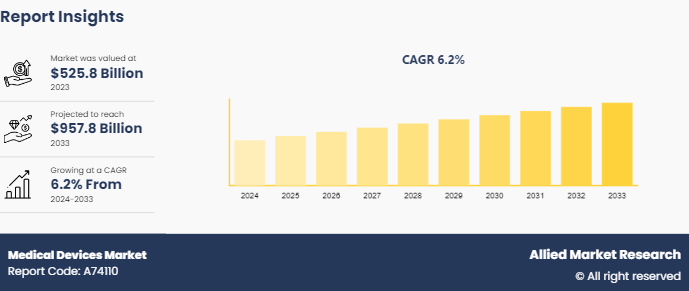

The global medical devices market size was valued at $525.8 billion in 2023, and is projected to reach $957.8 billion by 2033, growing at a CAGR of 6.2% from 2024 to 2033.

Market Introduction

Medical devices industry, encompassing a vast array of instruments, devices, and technologies, play an indispensable role in modern healthcare systems worldwide. Essential for diagnosis, treatment, monitoring, and prevention, these devices range from simple tools like tongue depressors to intricate implants such as pacemakers. With an estimated 2 million types available globally, they facilitate diverse medical procedures, from routine check-ups to complex surgeries. Their significance spans various settings, including home care, remote clinics, and advanced medical facilities. The World Health Organization emphasizes its pivotal role in advancing universal health coverage and responding to health emergencies. Despite their diversity, medical devices share a common goal which is to enhance patient care, improve health outcomes, and promote overall well-being.

Key Takeaways

- The medical devices market study covers 20 countries. The research includes a segment analysis of each country in terms of value ($billion) for the projected period from 2024 to 2033.

- More than 1, 500 product literatures, industry releases, annual reports, and other such documents of major medical devices industry participants along with authentic industry journals, trade associations' releases, and government websites have been reviewed for generating high-value industry insights.

- The study integrates high-quality data, professional opinions and analysis, and critical independent perspectives. The research approach intends to provide a balanced view of global markets and assist stakeholders in making informed decisions in order to achieve their most ambitious growth objectives.

Key Market Dynamics

The demand for medical devices is driven by various factors, including advancements in technology, increasing demand for improved healthcare outcomes, and the need for more efficient and effective diagnostic and treatment options. These devices play a crucial role in healthcare by enabling healthcare professionals to diagnose, monitor, and treat a wide range of medical conditions with greater accuracy and effectiveness. From simple tools like tongue depressors to sophisticated imaging machines and surgical robots, medical devices help to monitor vital signs, deliver medications, detect and diagnose diseases, and even support or replace damaged body parts.

The development and integration of medical devices face several notable limitations. Firstly, the regulatory process for introducing Class III medical devices, such as implantable, is rigorous and time-consuming, involving extensive technological and clinical testing. In addition, the inherently conservative nature of medicine often delays the adoption of new devices until controlled studies validate their efficacy.

The evolving landscape of medical devices presents numerous opportunities for the industry players to advance healthcare delivery. Miniaturization enables the development of wearable devices, facilitating convenient and continuous monitoring of vital signs. Wireless technology enhances data transmission, fostering remote monitoring, especially valuable during pandemics. Integration of artificial intelligence offers data analysis and pattern recognition, aiding in early detection of health issues. These factors are anticipated to have a positive impact on medical devices market forecast opportunities.

Global Medical Devices Market Opportunity Analysis

In 2022, the top medical device companies have showcased remarkable growth and innovation, solidifying their positions as industry leaders. Medtronic, with an impressive $30.12 billion in revenue, offers a diverse portfolio of cardiac rhythm disease, spine, cardiovascular, and diabetes management. Johnson & Johnson follows closely with $22.95 billion, boasting subsidiaries like DePuy Synthes, excelling in orthopedics and trauma care. Abbott, ranking third with $22.59 billion, is renowned for its diagnostics and cardiovascular devices. Philips, with $19.32 billion, specializes in clinical informatics and medical imaging systems.

In addition, GE Healthcare, generating $18.01 billion, excels in imaging and patient monitoring. BD, Siemens Healthineers, Cardinal Health, Stryker, and Baxter complete the top ten, each contributing significantly to the medical device landscape with innovative solutions spanning diagnostics, surgical equipment, orthopedic implants, and patient care products. These companies continue to drive advancements, enhancing healthcare delivery and patient outcomes globally. These factors are predicted to boost the medical devices market growth in the coming years.

Below are the top 10 medical device companies in the world in 2022 based on their revenue:

Company | Revenue ($Billion) |

Medtronic | $30.12 |

Johnson & Johnson Services, Inc. | $22.95 |

Abbott | $22.59 |

Koninklijke Philips N.V. | $19.32 |

GE Healthcare | $18.01 |

BD | $17.11 |

Siemens Healthineers AG | $16.93 |

Cardinal Health | $15.44 |

Stryker | $14.35 |

Baxter | $11.67 |

Market Segmentation

The medical devices market size is segmented into type, end user, and region. On the basis of type, the market is divided into orthopedic devices, diagnostic imaging, cardiovascular devices, wound management, minimally invasive surgical (MIS) , diabetes care, dental devices, ophthalmic devices, in vitro diagnostics (IVD) , general surgery, and others. Based on end user, the market is classified into hospitals & ambulatory surgery centers (ASCs) , clinics, and others. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Regional Market Outlook

In Europe, the medical devices market share continues to thrive, with over 34, 000 companies that have contributed around $161.9 billion (€150 billion) in 2021. Germany led with the highest number of medical technology companies, followed closely by Italy, the UK, France, and Switzerland. Remarkably, 95% of these companies were SMEs, with the majority employing fewer than 50 people. Despite comprising less than 1% of GDP, medical technology accounts for around 7.6% of healthcare spending in Europe. The European medical device market constitutes 27.3% of the global market. Over the past decade, the industry has seen steady growth, averaging 4.8% annually. Notably, Europe maintains a positive trade balance of $6.4 billion (€6 billion) , with key trade partners including the U.S., China, Japan, and Mexico.

Furthermore, Europe has the presence of leading medical device manufacturers. For instance, Siemens Healthineers, headquartered in Germany, is renowned for its cutting-edge diagnostic imaging and laboratory diagnostics equipment. Medtronic, based in Ireland, excels in producing a wide range of medical devices, from pacemakers to surgical tools. B. Braun, headquartered in Germany, specializes in medical instruments and pharmaceutical products. In addition, Philips Healthcare, headquartered in the Netherlands, is recognized for its advanced healthcare technology solutions, particularly in imaging and patient monitoring systems. These aspects are anticipated to drive the medical devices market growth in Europe.

Competitive Landscape

Some of the major players driving the medical devices market share include Medtronic, Johnson & Johnson Services, Inc., Siemens Healthineers AG, Abbott, Stryker, GE Healthcare, BD, Koninklijke Philips N.V., Cardinal Health, and Boston Scientific Corporation, and others.

Recent Key Strategies and Developments

- On May 14, 2024, Olympus, a company specializing in optics and imaging products unveiled new bronchoscopes compatible with the EVIS X1 Endoscopy System, offering enhanced imaging and procedural flexibility. The BF-H1100 and BF-1TH1100 bronchoscopes feature slimmer outer diameters and larger working channels for improved access to distal airways. With refined handling and advanced image sensors, they promise improved suction capabilities and reduced physical stress during procedures.

- On May 13, 2024, OMRON Healthcare India has joined forces with AliveCor India to introduce portable ECG monitoring devices in the Indian market. This collaboration expands OMRON's focus beyond hypertension management to include cardiovascular health. The partnership aims to enhance awareness and early detection of cardiovascular diseases (CVDs) by offering FDA-cleared home monitoring devices, such as OMRON COMPLETE, KardiaMobile, and KardiaMobile 6L.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the medical devices market analysis from 2023 to 2033 to identify the prevailing medical devices market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the medical devices market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

Apart from the points mentioned above, the report includes the analysis of the regional as well as global medical devices market trends, key players, market segments, application areas, and market growth strategies.

Industry Trends

- On May 10, 2024, FDA released final guidance on remanufacturing medical devices, addressing concerns raised by Advamed and other stakeholders. The updated document clarifies regulatory requirements for entities involved in servicing or remanufacturing, aiming to assist those less familiar with FDA rules. The guidance distinguishes between device servicing and remanufacturing, emphasizing changes to performance, safety, or intended use. It also provides clarity on modifications that significantly impact device specifications.

- On May 08, 2024, Samsung Medison announced its acquisition of Sonio, a French company specializing in AI software for fetal ultrasound exams, for approximately $92.4 million. Sonio's deep learning technology enhances image quality and supports fetal ultrasound examinations.

- On May 07, 2024, Medtronic gained approval from China's national medical products administration (NMPA) for its renal denervation system, Symplicity Spyral, marking a significant milestone in targeting China's high blood pressure population of over 245 million. The NMPA is tasked with ensuring the safety, quality, and efficacy of medical products available in the Chinese market.

Key Sources Referred

- National Institute of Health

- American Lung Association

- World Health Organization

- National Health Council

- U.S. Department of Health & Human Services

Medical Devices Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 957.8 Billion |

| Growth Rate | CAGR of 6.2% |

| Forecast period | 2024 - 2033 |

| Report Pages | 330 |

| By Type |

|

| By End User |

|

| By Region |

|

| Key Market Players | Stryker, Johnson & Johnson Services, Inc., Medtronic, Cardinal Health, Abbott, Siemens Healthineers AG, Koninklijke Philips N.V., GE Healthcare, Boston Scientific Corporation, BD |

Analyst Review

The medical devices market is trending towards wearable technology, telemedicine integration, AI-driven diagnostics, personalized medicine devices, and increased focus on cybersecurity and regulatory compliance.

North America is the largest regional market for medical devices industry.

The global medical devices market is estimated to reach $957.8 billion by 2033

The top companies that hold considerable share in medical devices market are Medtronic, Johnson & Johnson Services, Inc., Siemens Healthineers AG, Abbott, Stryker, GE Healthcare, BD, Koninklijke Philips N.V., Cardinal Health, and Boston Scientific Corporation.

Loading Table Of Content...