Non Vascular Stent Market Research, 2035

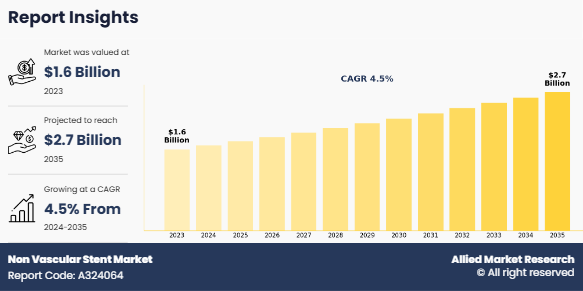

The global non vascular stent market size was valued at $1.6 billion in 2023, and is projected to reach $2.7 billion by 2035, growing at a CAGR of 4.5% from 2024 to 2035.The non vascular stent market is expanding, driven by rise in prevalence of chronic diseases. According to the Centers for Disease Control and Prevention (CDC), six in ten adults in the U.S. were affected by chronic conditions in 2023. Rise in health prevalence is boosting the demand for advanced medical devices, particularly non vascular stents, to manage associated complications effectively. These stents are extensively used in gastrointestinal, urological, and pulmonary cases, meeting the growing demand for effective, minimally invasive treatment options.

Stents are tubular medical devices designed to keep passageways in the body open, typically used to treat obstructions or narrowing. They can be vascular, placed in blood vessels, or non vascular, used in lumens like the gastrointestinal, biliary, urinary, or respiratory tracts. Non vascular stents work by providing structural support to maintain patency in blocked or narrowed passages. They are deployed using minimally invasive techniques such as endoscopy or fluoroscopy and expand to the desired size, either through self-expansion or balloon dilation. Made from materials such as nitinol (a shape-memory alloy), stainless steel, polymers, or biodegradable substances, non vascular stents feature coatings to reduce inflammation or prevent infection. These stents alleviate symptoms, improve organ function, and enhance quality of life.

Key Takeaways

- On the basis of product type, the urological stents segment dominated the non vascular stent market size in 2023. However, the pulmonary (airway) stents segment is anticipated to grow at the highest CAGR during the non vascular stent market forecast period.

- On the basis of material type, the non-metallic stents segment dominated the market share in 2023 and is anticipated to grow at the highest CAGR during the forecast period.

- On the basis of end user, the hospitals segment dominated the market share in 2023. However, the others segment is anticipated to grow at the highest CAGR during the forecast period.

- Region wise, North America generated the largest revenue in 2023. However, Asia-Pacific is anticipated to grow at the highest CAGR during the forecast period.

Market Dynamics

The non vascular stent market is experiencing substantial growth, driven primarily by rise in prevalence of chronic diseases worldwide. Among these, esophageal cancer serves as a prominent example, highlighting the urgent need for advanced medical interventions. According to the American Cancer Society, the lifetime risk of developing esophageal cancer in the U.S. is approximately 1 in 127 for men and 1 in 434 for women. Such alarming statistics reflect the increasing prevalence of chronic diseases that necessitate advanced treatment options like non vascular stents. These stents play a crucial role in managing a variety of conditions, including those that cause obstructions or strictures, which are common in gastrointestinal and pulmonary diseases. With rise in number of patients suffering from chronic ailments, the demand for non vascular stents, which offer long-term solutions, is also rising.

The adoption of minimally invasive procedures is another major contributor to the market's expansion. Minimally invasive techniques, including endoscopic stent placement, are becoming increasingly popular among both patients and healthcare providers. These procedures are less invasive than traditional surgical methods, which results in shorter recovery times, reduced hospital stays, and fewer complications. For patients, this translates into an enhanced quality of life and faster recovery, which makes minimally invasive procedures a highly preferred option. The growing shift towards these methods is directly fueling the demand for non vascular stents, as they are essential tools in performing such procedures. This transition to minimally invasive treatments is likely to continue as healthcare providers prioritize patient outcomes and cost-effective solutions.

Moreover, the involvement of key players in the development of advanced non vascular stents is further accelerating the non vascular stent market growth. Leading medical device companies are continuously innovating, focusing on improving stent materials, designs, and functionality to cater to the specific needs of different patient groups. For instance, development of self-expanding stents, biodegradable stents, and MRI-compatible stents has enhanced their clinical application and effectiveness. The introduction of these advanced stents has significantly expanded their role in medical treatments, attracting more healthcare providers to adopt them. In addition, availability of reimbursement options is crucial in promoting the widespread use of non vascular stents. With insurance coverage supporting the cost of these devices, patients can access them more easily, thereby increasing market adoption.

However, the non vascular stent market does face certain challenges that could hinder its growth. The high cost of advanced stents, combined with stringent regulatory requirements for product approval, may limit their accessibility, especially in low-income regions. Regulatory hurdles often delay the time-to-market for new products, restricting patient access to the latest treatment options.

Despite these challenges, the ongoing advancements in technology, such as MRI-compatible non vascular stents, are helping overcome some of these barriers. These stents, which allow for better compatibility with diagnostic imaging, enhance the accuracy of treatments and improve overall patient care. As the demand for non vascular stents continues to rise, these technological innovations are likely to support sustained non vascular stent market growth, improving patient outcomes and expanding the scope of stent-based treatments globally.

Segmental Overview

The non vascular stent industry is segmented into product type, material type, end user, and region. On the basis of product type, it is segmented into gastrointestinal stents, pulmonary (airway) stents, urological stents, and others. On the basis of material type, the market is classified into metallic stents, and non-metallic stents. On the basis of end user, it is classified into hospitals, ambulatory surgical centers, and others. On the basis of region, the market is segmented into North America, Europe, Asia-Pacific, and LAMEA.

By Product Type

By product type, the urological stents segment dominated the non vascular stent market share in 2023. This was attributed to the rising prevalence of urological disorders such as kidney stones, ureteral strictures, and benign prostatic hyperplasia (BPH). The increasing adoption of minimally invasive procedures, advancements in stent design improving biocompatibility and durability, and growing awareness among healthcare professionals further contributed to its market leadership.

However, the pulmonary (airway) stents segment is expected to register the highest CAGR during the forecast period owing to the rising prevalence of respiratory disorders, such as chronic obstructive pulmonary disease (COPD) and tracheal stenosis, is a key factor propelling this segment's growth. The increasing adoption of minimally invasive treatments, heightened awareness of airway management solutions, and innovations in stent designs specifically developed for respiratory applications further contribute to the market expansion.

By Material Type

By material type, the non-metallic stent segment dominated the non vascular stent market share in 2023. This was attributed to the rising demand for biodegradable and polymer-based stents is driven by their ability to reduce long-term complications such as inflammation and migration. Their capacity to offer temporary support without necessitating removal makes them highly appealing to both patients and healthcare providers. Additionally, the growing emphasis on patient-centric care, advancements in material technologies, and expanding applications further boost the adoption of non-metallic stents.

By End User

By end user, the hospitals segment dominated the market in 2023, owing to their advanced infrastructure, skilled medical personnel, and expertise in performing complex procedures, such as precise stent placement. Hospitals deliver a comprehensive array of services and are equipped with cutting-edge technologies for diagnosing and treating conditions that require non vascular stents. Moreover, they offer superior access to post-procedure care and management, solidifying their leading position in the market.

However, the others segment is expected to register the highest CAGR during the forecast period owing to increasing clinical research activities, advancements in stent technologies, and growing collaborations between healthcare institutions and manufacturers. Specialty clinics offer specialized treatments, driving demand for advanced stents, while research institutes contribute to innovation and new product development. Additionally, the rising focus on personalized medicine and the increasing number of academic studies on non-vascular stents further support market growth.

By Region

Region wise, North America was the largest shareholder in the non vascular stent market in 2023, owing to its well-established healthcare infrastructure, advanced medical technology, and high healthcare expenditure. The presence of leading market players, favorable reimbursement policies, and a growing aging population further contributed to the region's dominance. Additionally, North America's strong research and development capabilities, along with high awareness and adoption of minimally invasive procedures, fueled the market's growth.

However, Asia-Pacific is anticipated to register the highest CAGR during the forecast period owing to the region's rapidly growing healthcare infrastructure, rising prevalence of chronic diseases, and increasing demand for minimally invasive treatments. The aging population, coupled with rising awareness and affordability of advanced medical technologies, drives market adoption. Additionally, government initiatives to expand healthcare access and investments in medical device innovation are expected to further accelerate market growth in the region.

Competition Analysis

Competitive analysis and profiles of the major players in the ELLCS, s.r.o., Boston Scientific Corporation, Hobbs Medical Inc, Becton, Dickinson & Company, W.L. Gore & Associate Inc, Medtronic Plc, MICRO-TECH (Nanjing) Co., Ltd., Q3 Medical Group, CONMED Corporation, and Cook Medical. The key players have adopted product approval as the key strategies for expansion of their product portfolio.

Recent Developments in Non Vascular Stent Industry

- In March 2021, AMG International GmbH, a subsidiary of Q3 Medical Devices Limited, strengthened its leadership in biodegradable implant development. The company received CE Mark approval for its UNITY-B balloon-expandable biodegradable biliary stent (BEBS), designed for endoscopic use. This new product complements the ARCHIMEDES biodegradable pancreaticobiliary stent, the worlds first CE-approved biodegradable implant. The UNITY-B, alongside ARCHIMEDES, offers a range of degradation profiles, including fast, medium, and long-lasting options, addressing varying clinical needs.

Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the non vascular stent market analysis from 2023 to 2035 to identify the prevailing non vascular stent market opportunity.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the non vascular stent market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global non vascular stent market trends, key players, market segments, application areas, and market growth strategies.

Non Vascular Stent Market Report Highlights

| Aspects | Details |

| Market Size By 2035 | USD 2.7 billion |

| Growth Rate | CAGR of 4.5% |

| Forecast period | 2023 - 2035 |

| Report Pages | 285 |

| By Material Type |

|

| By End User |

|

| By Product Type |

|

| By Region |

|

| Key Market Players | Hobbs Medical Inc., Medtronic plc, Cook Group, Becton, Dickinson, and Company, W.L. Gore & Associate Inc., Micro-tech (nanjing) Co., Ltd., Boston Scientific Corporation, CONMED Corporation, Q3 Medical Group, ELLA – CS, s.r.o. |

Analyst Review

This section provides various opinions of top-level CXOs in the non vascular stent market. According to CXO insights, the market growth is primarily driven by increase in prevalence of chronic diseases, rise in preference for minimally invasive procedures, and advancements in stent materials, including biodegradable options. CXOs highlight that rise in adoption of non vascular stents in palliative care and their expanded applications in conditions like biliary and gastrointestinal obstructions further support market expansion.

CXOs also emphasized that favorable reimbursement policies and increased awareness among healthcare professionals about the benefits and applications of non-vascular stents contribute to their broader adoption. However, they pointed out that high procedural costs, complications like stent migration, and stringent regulatory frameworks pose significant challenges to market growth.

North America dominates the market due to its advanced healthcare infrastructure, strong adoption of innovative medical devices, and favorable reimbursement systems. However, the Asia-Pacific region is expected to witness the highest CAGR during the forecast period, driven by rise in aging population, rise in incidence of chronic diseases, and increase in investments in healthcare infrastructure and minimally invasive technologies.

The total market value of non vascular stent Market was $ 1.6 billion in 2023.

The market value of non vascular stent Market is projected to reach $ 2.7 billion by 2035.

The forecast period for non vascular stent Market is 2024 to 2035

The base year is 2023 in non vascular stent Market.

Non vascular stents work by providing structural support to maintain patency in blocked or narrowed passages. They are deployed using minimally invasive techniques such as endoscopy or fluoroscopy and expand to the desired size, either through self-expansion or balloon dilation. Made from materials such as nitinol (a shape-memory alloy), stainless steel, polymers, or biodegradable substances, non vascular stents often feature coatings to reduce inflammation or prevent infection. These stents alleviate symptoms, improve organ function, and enhance quality of life.

Loading Table Of Content...

Loading Research Methodology...