Table Of Contents

Lalit Janardhan Katare

Koyel Ghosh

Aerospace and Defense Domain: Analyzing the Top 5 Emerging Markets Influencing the Growth of the Sector in Q4 2024

In the last few years, there has been a huge rise in geopolitical tensions with numerous conflicts emerging across the globe, including the Russia-Ukraine war, Israel-Palestine clashes, India-China border skirmishes, etc. Additionally, the number of terrorist attacks has increased exponentially around the world, putting the safety and security of citizens and critical infrastructure at risk. In such a scenario, several developed and developing countries have invested heavily in advanced military technologies to boost the capabilities of their defense forces. Moreover, the entry of private players in space exploration activities has broadened the scope of the aerospace and defense domain. Recently, Allied Market Research, using its in-house ‘Title Matrix Tool’, has published a study on the top 5 emerging markets in the sector. Each of these markets is studied comprehensively in the report, with extensive focus on its growth drivers and investment opportunities.

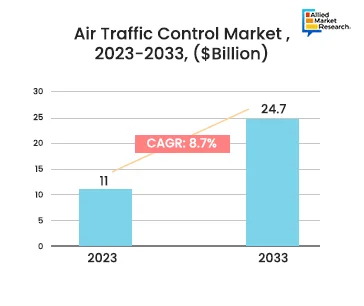

Air Traffic Control Market

Air traffic control includes a set of advanced technologies, systems, infrastructure, and services that are deployed for better management and regulation of air traffic. As per the AMR report on the air traffic control market, the industry accounted for $11.0 billion in 2023. The study further adds that the landscape is projected to gather a revenue of $24.7 billion by 2033, rising at a CAGR of 8.7% during 2024-2033. The overall rise in demand for air travel is expected to be the primary reason behind the growth of the landscape in the coming period. Moreover, technological advancements and innovations in aviation infrastructure have impacted the industry positively in the fourth quarter of 2024. The emergence of next-generation telecommunication mechanisms has also played a role in the expansion of the industry.

The presence of several multinational giants, including L3Harris Technologies Inc. (U.S.), the Westminster Group Plc. (UK), Kongsberg Defence & Aerospace (Norway), Raytheon Technologies (U.S.), National Air Traffic Services (NATS) (UK), etc., has broadened the scope of the industry. Many of these companies have been actively engaged in R&D activities to design and manufacture state-of-the-art aviation traffic control systems. The launch of ingenious products by these players and the strategic alliances established by various enterprises have strengthened the foothold of the landscape. Along with this, several governments have launched initiatives to modernize their airports and other infrastructure projects, thereby augmenting the growth rate of the market. The advent of satellite-based navigation systems has further improved the quality of air traffic control systems, increasing their adoption in various countries.

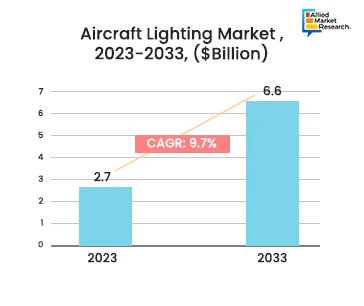

Aircraft Lighting Market

Allied Market Research recently issued a report on the aircraft lighting market which highlights that the industry, which accounted for $2.7 billion in 2023, is predicted to gather a revenue of $6.6 billion by 2033, rising at a CAGR of 9.7% during 2024-2033. A substantial increase in new aircraft production by major companies in the landscape has helped the market flourish in Q4 2024. Aircraft lighting systems are extremely important for the overall safety and visibility of the airplane. In the last few years, with a spike in air accidents, several countries around the world enacted laws and regulations mandating the use of these lighting systems. As a result, leading companies such as Boeing, Air India, Airbus, etc., are partnering with electronics and IT companies to install lighting solutions in their existing fleets. Moreover, innovations in OLED and LED devices have created new investment opportunities in the industry.

The AMR study also provides an in-depth analysis of the performance of the industry in various regions across the globe including North America, LAMEA, Europe, and Asia-Pacific. All the significant administrative, cultural, demographic, socioeconomic, and political factors influencing the landscape in these provinces are covered extensively. The Asia-Pacific region has witnessed huge growth in the demand for air travel from developing countries such as China, India, Indonesia, Vietnam, etc. At the same time, the increasing focus of US-based companies on innovation and technological upgrades has improved the growth rate of the market in North America. Naturally, both these regions have dominated the industry in the last few years and are expected to gather a huge revenue share in the near future.

In-Space Manufacturing, Servicing, and Transportation Market

The in-Space Manufacturing, Servicing, and Transportation (ISMST) Market is a comprehensive industry segment that deals with the design, development, repair, and maintenance of space equipment. The gradual transition toward additive manufacturing techniques such as 3D printing has contributed to the growth of the industry in the fourth quarter of 2024. Additionally, the production of autonomous systems has created numerous growth opportunities in the market. Previously, there were a lot of regulatory uncertainties and policy constraints that restricted the entry of private companies in space exploration activities. However, in the last few years, many countries have enacted laws to allow the entry of such enterprises, thereby expanding the footprint of the landscape. As per a report on the in-space manufacturing, servicing, and transportation market by AMR, the industry is expected to amass a sum of $561.5 billion by 2033, citing a CAGR of 8.2% during 2024-2033.

The AMR report highlights that the in-space manufacturing, servicing, and transportation market is expected to witness huge growth in the North America region in the coming period. The increasing investments by the US government in their NASA Artemis program have played a key role in the expansion of the industry in the province. Along with this, companies such as SpaceX, Blue Origin, etc., have made significant gains in the last few years, thereby accelerating the market’s growth rate. Moreover, governmental entities such as the European Space Agency, Indian Space Research Organization, JAXA, etc., have contributed to the growth of the landscape in other regions such as Europe and Asia-Pacific.

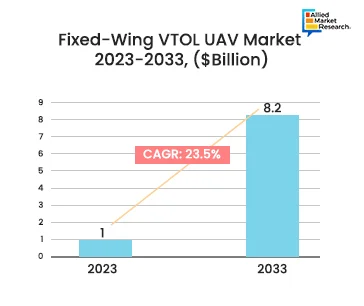

Fixed-Wing VTOL UAV Market

According to a report published by Allied Market Research, the fixed-wing VTOL UAV market is expected to register a revenue of $8.2 billion by 2033. The industry accounted for $1.0 billion in 2023, growing at a CAGR of 23.5% during 2024-2033. The long-distance endurance and high-speed capabilities of fixed-wing UAVs make them ideal for several applications, including disaster response, agriculture monitoring, infrastructure supervision, military reconnaissance, etc. The rising applicability of these drones in different end-use sectors is predicted to help the industry flourish in the near future. Furthermore, the emergence of AI and ML has presented companies with numerous opportunities to integrate these innovations into drones, thereby impacting the market positively. Also, companies are increasingly adopting these solutions as they are quite affordable as compared to traditional manned aircraft.

Over the years, the pace of urbanization and industrialization has surged significantly, especially in countries such as India and China. Many companies in these countries have launched initiatives to give a boost to urban infrastructure, agriculture, disaster management technologies, etc. These programs have, in turn, increased the utility of UAVs in these sectors. Countries such as China have also developed specialized drones for military purposes, including surveillance, combat operations, and reconnaissance. As a result of these heavy investments, the fixed wing VTOL UAV market is predicted to witness huge growth in the Asia-Pacific region. Also, the launch of several innovative products by US-based multinational corporations has broadened the scope of the landscape in North America.

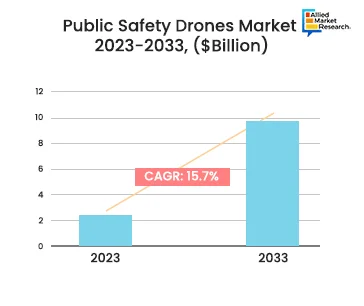

Public Safety Drones Market

Public safety drones are unmanned aerial vehicles used by governmental organizations such as law enforcement agencies, medical service providers, and fire departments for emergency response. These UAVs are generally equipped with advanced sensors, cameras, and data-capturing devices to assist quick response teams in rescue operations. Over the years, these drones have proven to be extremely efficient in disaster management operations. Studies have shown that the use of drones has reduced the casualty rate drastically, thus ensuring the safety of civilians and personnel. As per the report by AMR, the public safety drones market is anticipated to amass a revenue of $9.9 billion by 2033. The industry accounted for $2.3 billion in 2023 and is expected to rise at a CAGR of 15.7% during 2024-2033.

In the last few years, technological advancements in consumer electronics and semiconductor manufacturing have led to the development of advanced sensors and thermal imaging devices. Drone manufacturers are producing state-of-the-art UAVs that have enhanced situational awareness and are capable of performing various tasks. The integration of AI and ML algorithms has further opened new avenues for growth in the industry. Many countries in Latin America and Asia-Pacific have promoted the use of these drones in public safety agencies, thus helping the industry improve its revenue share in these regions. Public safety drones played an important role during the COVID-19 pandemic by delivering essential medicines and drugs to different hospitals and clinics. In the post-pandemic period, many emergency medical service providers have started using UAVs for various tasks, contributing to the global growth of the industry.

Winding up

In conclusion, the aerospace and defense domain has expanded significantly in the past few years due to the increasing number of geopolitical conflicts and technological advancements in semiconductor and electronics manufacturing. The AMR reports on the top 5 emerging markets throw light on the different factors influencing the overall growth of the sector, thereby aiding companies in formulating comprehensive growth strategies in the long run.

For insights into the upcoming trends and latest advancements in the aerospace and defense domain, contact our experts.