Solar Fuel Market Research, 2033

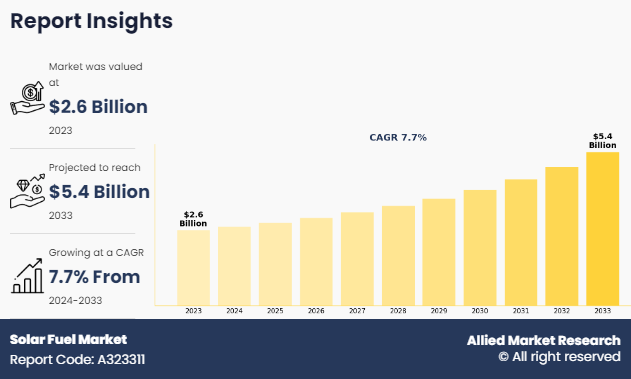

The global solar fuel market was valued at $2.6 billion in 2023, and is projected to reach $5.4 billion by 2033, growing at a CAGR of 7.7% from 2024 to 2033. The global solar fuel market is experiencing growth due to several factors such as an increase in the importance of sustainability, advancements in solar energy technology, and growing investments in green hydrogen projects. However, the high initial investment costs, and lack of widespread infrastructure limit the market expansion. However, the rise in demand for renewable energy solutions, the shift towards green hydrogen production, and government initiatives to invest in solar fuel development provide lucrative opportunities for solar fuel market growth.

Introduction

Solar fuels harness sunlight to drive chemical reactions that convert water and carbon dioxide into energy-rich compounds like hydrogen or synthetic hydrocarbons. This innovative approach offers a promising solution to mitigate greenhouse gas emissions and reduce dependency on fossil fuels. With the increase in global focus on sustainability and the imperative to combat climate change, the solar fuel market is gaining traction as a vital component of the transition towards a cleaner, greener energy future.

Market Dynamics

The increase in the importance of sustainability is driving the solar fuels market by fostering a global shift towards cleaner energy sources. As major countries prioritize environmental responsibility, demand for renewable alternatives grows in comparison with traditional fossil fuels. Advancements in solar energy technology play a crucial role by enhancing the efficiency and scalability of solar fuel production, making it a more economically viable and attractive option for power generation, and others. In addition, growing investments in green hydrogen projects signal a commitment to developing sustainable energy infrastructure, further stimulating innovation and market expansion in the solar fuels sector. The abovementioned driving factors propel the adoption of solar fuels as a key solution in the transition towards a more sustainable energy future.

The high initial investment costs pose a significant barrier to entry for individuals and organizations looking to invest in solar fuel technology. These costs encompass the development and deployment of solar energy infrastructure, as well as research and development expenses for innovative technologies. For many potential investors, especially smaller companies or developing nations, the upfront capital required may be prohibitive, slowing down the adoption and growth of solar fuels.

In addition, the lack of widespread infrastructure presents challenges in terms of distribution and scalability. Lack of a well-established infrastructure for solar fuel production, transportation, and storage, the market faces limitations in reaching broader consumer bases and achieving economies of scale. This lack of infrastructure hampers the commercial viability of solar fuels and deters investors who are hesitant to enter a market with uncertain logistical challenges. The abovementioned restraining factors limit the rapid expansion of the solar fuels market by limiting access to capital and hindering the development of necessary infrastructure for widespread adoption and integration into existing energy systems.

The shift towards green hydrogen production presents a significant opportunity for the solar fuels market by creating a growing demand for renewable hydrogen, a key component of solar fuels. As industries and governments worldwide prioritize decarbonization efforts, green hydrogen produced through solar fuel technologies emerges as a viable solution to meet this demand sustainably. This shift not only drives investment and innovation in solar fuel production but also fosters market growth by expanding the application and adoption of solar fuel technologies across various sectors.

Furthermore, the expansion of solar fuel infrastructure offers another opportunity for market development. As infrastructure improves to support the production, storage, and distribution of solar fuels, it enhances the scalability and accessibility of these renewable energy sources. This expansion facilitates the integration of solar fuel technologies into existing energy systems, enabling broader deployment and utilization. In addition, a robust infrastructure network reduces barriers to entry for new market players and encourages further investment, ultimately driving the growth and maturation of the solar fuels market.

Segments Overview

The solar fuel market is segmented into type, application, and region. On the basis of type, the market is divided into hydrogen, hydrazine, ammonia, and others. On the basis of application, the market is bifurcated into transportation, power generation, and others. On the basis of region, the solar fuel market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

On the basis of type, the hydrogen segment dominates the solar fuel market size due to its versatility, growing demand, supportive market conditions, and technological advancements. Hydrogen is a clean, versatile energy carrier with applications in transportation, electricity generation, and industrial processes. Government support and regulations encourage investment in green hydrogen projects. Advancements in solar energy technology, such as photovoltaics and concentrated solar power, improve efficiency and cost-effectiveness, making hydrogen a key driver towards a sustainable energy future. According to IEA Global Hydrogen Review 2023, “IEA predicts that renewable capacity for hydrogen will reach 45 GW by 2028, however, the abovementioned data only represents only 7% of the announced capacity for the same period.”

Electrochemical processes, such as electrolysis, offer a direct pathway to harness solar energy and convert it into storable and transportable fuels such as hydrogen or synthetic hydrocarbons. One key advantage of electrochemical technologies is their high efficiency in converting solar energy into fuel, often surpassing other methods. In addition, these processes can be easily scaled up to meet varying energy demands, from small-scale applications to large industrial operations. Moreover, electrochemical methods offer flexibility in the choice of feedstocks, allowing for the use of readily available resources such as water or carbon dioxide. This versatility enhances the attractiveness of electrochemical technologies for sustainable fuel production.

According to IEA tracking clean energy progress in 2023, “Electrochemical and electrolysis are critical technology for the production of low-emission hydrogen from renewable or nuclear electricity. Electrolysis capacity for dedicated hydrogen production has been growing in the past few years, but the pace slowed down in 2022 with about 130 MW of new capacity entering operation, 45% less than the previous year. However, electrolyzer manufacturing capacity increased by more than 25% since last year, reaching nearly 11 GW per year in 2022. The realization of all the projects in the pipeline is expected to lead to an installed electrolyzer capacity of 170-365 GW by 2030. Electrolysis capacity is growing from a low base and requires a significant acceleration to get on track with the Net Zero Emissions by 2050 (NZE) Scenario, which requires installed electrolysis capacity to reach more than 550 GW by 2030.”

On the basis of application, the transportation segment dominates the solar fuel market forecast primarily due to its significant reliance on liquid fuels for mobility, which can be effectively addressed by solar fuel industry technologies. Solar fuels, such as hydrogen or synthetic hydrocarbons, offer a sustainable alternative to traditional fossil fuels for various transportation modes, including cars, trucks, buses, ships, and airplanes. One key advantage is that solar fuels can be produced using renewable energy sources like solar power, making them carbon-neutral or even carbon-negative depending on the production process. This aligns well with the transportation sector's increasing focus on reducing greenhouse gas emissions and achieving sustainability targets.

In addition, solar fuels can leverage existing infrastructure for fuel distribution and utilization, minimizing the need for extensive infrastructure upgrades or modifications. This makes them more readily adoptable within the transportation sector, where infrastructure compatibility and convenience are crucial considerations. Furthermore, advancements in solar fuel production technologies and decreasing costs are making solar fuels competitive with conventional fossil fuels. As a result, the transportation sector sees solar fuels as a viable solution to reduce its carbon footprint and transition towards cleaner energy sources, driving the dominance of the transportation segment in the solar fuels market.

According to IEA’s Net Zero Emission (NZE) by 2050 Scenario “Hydrogen from renewables falls to as low as USD 1.3 per kg by 2030 in regions with excellent renewable resources (range USD 1.3-3.5 per kg), comparable with the cost of hydrogen from natural gas with CCUS. In the longer term, hydrogen costs from renewable electricity fall as low as USD 1 per kg (range USD 1.0-3.0 per kg) in the NZE Scenario, making hydrogen from solar PV cost-competitive with hydrogen from natural gas even without CCUS in several regions.”

On the basis of region, Asia-Pacific dominates the solar fuel market share primarily due to several key factors. For instance, the region boasts abundant solar resources, making it conducive to solar energy generation and consequently solar fuel production. Countries like China, India, and Japan have made substantial investments in solar energy infrastructure and research, driving technological advancements and market growth. In addition, rapid industrialization and urbanization in Asia-Pacific have led to heightened energy demand and increased pressure to reduce carbon emissions. As a result, governments in the region are implementing policies and incentives to promote renewable energy adoption, including solar fuels.

Furthermore, Asia-Pacific is home to some of the world's largest economies and energy markets, providing a significant market opportunity for solar fuel technologies. The region's strong manufacturing base and technological expertise also contribute to its dominance in the solar fuel market, with companies and research institutions driving innovation and commercialization efforts.

According to IEA Renewable 2023: Analysis and Forecast 2028, “It predicts that 24GW of renewable energy capacity will be installed for hydrogen production in China by 2028, “far above the estimated 1GW needed” to power the central government’s ambition for 100,000-200,000 tons/year of renewable H2 by 2025.”

Competitive Analysis

The major players operating in the solar fuels market include Green Hydrogen Systems, Air Liquide, Adani Green Energy Ltd, Royal Dutch Shell, Plug Power Inc., GAIL (India) Limited, Ballard Power Systems, NTPC Limited, Reliance Industries, and Linde Plc.

Policies and Key Regulations

U.S.: In 2021, the US Congress passed the Bipartisan Infrastructure Law, which includes grants for the creation of hydrogen hubs, with selected projects due to be announced in Q3 2023, and incentives to foster infrastructure and electrolysis manufacturing. The IRA, signed in August 2022, offers several tax credits and grant funding to support hydrogen technologies, with an expected impact on electrolyzer deployment and manufacturing facilities.

European Union: In July 2022, the European Commission approved funding of EUR 5.4 billion to support its first hydrogen-related Important Project of Common European Interest (IPCEI), with a focus on hydrogen technologies. In February 2023, the Commission adopted the Delegated Act defining production criteria for hydrogen to be considered renewable. In March 2023, the EU Hydrogen Bank was launched, to cover the initial green premium for renewable hydrogen, both produced inside the EU and imported.

Germany: In 2021, Germany launched the H2Global initiative, which uses a mechanism analogous to the carbon contracts for difference (CCfD) approach, compensating the difference between supply and demand prices with grant funding from the German government. The bidding process was launched in December 2022, with deliveries expected for the end of 2024, although tender deadlines have recently been extended.

UK: In 2021 the UK presented a business model for low-carbon hydrogen, based on a similar approach to CCfDs, that went through public consultation in 2022. Between July 2022 and January 2023, the government opened the first Electrolytic Allocation Round and pre-selected projects, intending to support at least 250 MW of capacity. The second allocation round opened by the end of 2023.

Key Benefits For Stakeholders

- This solar fuel market report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the solar fuel market analysis from 2023 to 2033 to identify the prevailing solar fuel market opportunities.

- The solar fuel market statistics research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the solar fuel market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global solar fuel market outlook.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global solar fuel market trends, key players, market segments, application areas, and market growth strategies.

Solar Fuel Market Report Highlights

| Aspects | Details |

| Market Size By 2033 | USD 5.4 billion |

| Growth Rate | CAGR of 7.7% |

| Forecast period | 2023 - 2033 |

| Report Pages | 290 |

| By Type |

|

| By Application |

|

| By Region |

|

| Key Market Players | GAIL (India) Limited, Linde Plc., Reliance Industries, Air Liquide, NTPC LIMITED, Plug Power Inc.,, Green Hydrogen Systems, Adani Green Energy Ltd, Ballard Power Systems, Royal Dutch Shell PLC |

Analyst Review

The solar fuel market is experiencing exponential growth, driven by various factors that boost its emergence as a key player in the global energy landscape. Sustainability imperatives, exacerbated by escalating greenhouse gas emissions from transportation and power generation sectors, have propelled solar fuel technologies to the forefront.

With mounting concerns over carbon emissions, governments worldwide are enacting stringent policies and regulatory guidelines aimed at curbing environmental degradation. Non-compliance often incurs penalties, incentivizing industries to explore renewable energy alternatives such as solar fuels.

In addition to regulatory pressures, significant advancements in solar energy utilization for fuel production have spurred market momentum. Breakthrough experiments and record-setting achievements in sustained solar energy conversion into fuels have galvanized substantial investments from both private and public sectors. Green hydrogen projects, in particular, have garnered considerable attention, further propelling market expansion.

According to McKinsey Hydrogen Outlook forecast suggests a promising trajectory for green hydrogen, with projections indicating that it is expected to capture over 70% of the hydrogen market share by 2050, eclipsing other hydrogen production methods. This shift underscores a broader transition towards renewable energy sources and underscores the pivotal role of solar fuels in achieving decarbonization goals.

The momentum is evident, with over 1000 solar fuel projects announced globally in 2023 alone, boasting a cumulative investment valuation exceeding $320 billion. This influx of investment boosts growing confidence in the viability and potential of solar fuel technologies to drive sustainable energy transitions on a global scale.

As the solar fuel market continues to evolve and mature, its transformative impact on energy systems becomes evident. With a growing emphasis on sustainability and renewable energy adoption, solar fuels are expected to play a pivotal role in shaping a cleaner, greener future for generations to come.

$5.4 billion is the estimated industry size of solar fuel market in 2033.

Green Hydrogen Investment Technological Advancements in Solar-to-Fuel Conversion Infrastructure Expansion Policy and Regulatory Support Strategic Partnerships and Collaborations are the upcoming trends of Solar Fuel Market in the world.

Power Generation is the leading application of Solar Fuel Market in 2023.

Europe is the largest regional market for solar fuel in 2023.

Green Hydrogen Systems, Air Liquide, Adani Green Energy Ltd, Royal Dutch Shell, Plug Power Inc., GAIL (India) Limited, Ballard Power Systems, NTPC Limited, Reliance Industries, and Linde Plc. are the top companies to hold the market share in Solar Fuel.

Loading Table Of Content...

Loading Research Methodology...