Sports Training Market Research, 2035

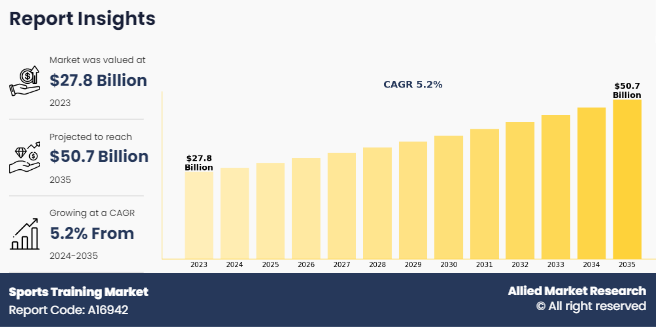

The global sports training market size was valued at $27.8 billion in 2023 and is projected to reach $50.7 billion by 2035, growing at a CAGR of 5.2% from 2024 to 2035. Sports training is a systematic process aimed at improving athletic performance through planned physical exercises, skill development, and psychological preparation. It consists of various components, including strength, endurance, flexibility, speed, and coordination. Effective sports training involves periodization, where training intensity and volume are varied to optimize performance and prevent injuries. It integrates specific drills, conditioning programs, and recovery strategies tailored to an athlete’s needs and goals. Coaches and sports scientists often utilize data and technology to monitor progress and adjust. Ultimately, sports training aims to enhance the capability and achieve peak performance of individuals in a particular sport.

Market Dynamics

The sports training market has experienced rapid expansion in recent years owing to several factors. One of them is the rise in sports participation rates, which has significantly boosted the demand for the sports training market by creating a larger pool of individuals seeking to enhance their athletic skills and performance. According to Sports Destination Management, 242 million Americans, which consisted 80% of people aged 6 and older, participated in sports or fitness activities in 2023, a 2.2% increase from 2022. With 5 million new participants in 2023 and continuous growth over the past decade, the sports training industry is anticipated to experience an increased demand for its services and products. Moreover, as more people engage in sports, from recreational athletes to professionals, the need for specialized training programs, coaching services, and advanced training equipment increases. The surge in demand is driven by a desire to improve fitness levels, prevent injuries, and achieve competitive success, which in turn fuels the growth of businesses providing sports training solutions.

In addition, the increase in sports participation also stimulates demand for innovative training technologies and methods. With more athletes aiming to optimize their performance, there is a greater market for products such as wearable fitness trackers, performance analysis software, and virtual training platforms. Companies that offer these cutting-edge solutions benefit from the growing trend, as they cater to the evolving needs of athletes seeking efficiency and effectiveness in their training regimes. The dynamic market expansion supports the development of new sports training products and also encourages continuous advancements and investments in the sector, which ensures sustained growth and competitiveness.

However, the market faces certain challenges in the sports training market growth. The high cost of sports training software acts as a significant restraint on market demand within the sports training industry. Many training programs and academies, especially smaller ones or those in developing regions, find it financially challenging to invest in expensive software solutions. These tools often require substantial upfront costs for licensing, installation, and ongoing maintenance, which can strain budgets already allocated to other essential resources such as coaching staff and equipment. For instance, advanced performance analysis software used in professional sports requires specialized hardware and software integration, which adds to the overall expense. Similarly, virtual coaching platforms that offer real-time feedback and video analysis come with high subscription fees and customization costs, limiting access for smaller organizations or amateur athletes.

Moreover, the high cost of sports training software can deter potential clients and athletes from participating in training programs, especially in economically constrained regions or among demographics with limited financial resources. The disparity in access to cutting-edge training technology can widen the performance gap between well-funded and less-funded teams or individuals, potentially hindering overall sports training market growth. Thus, the prohibitive cost remains a significant barrier to widespread adoption and market expansion across various sectors of the sports training industry.

Furthermore, the integration of artificial intelligence (AI) and machine learning into sports training has transformed the industry, creating numerous opportunities for the market players in the coming years. These technologies have enabled the development of highly personalized training programs, real-time performance analysis, and predictive modeling for injury prevention. AI-powered systems can process vast amounts of data from various sources, including wearable devices, video footage, and historical performance metrics, to provide insights that were previously impossible to obtain. Such developments using AI have led to more efficient training methods, improved athlete performance, and a growing market for AI-driven sports training solutions.

Recent launches in the sports training market highlight the rapid advancements and market potential. For instance, Sparta Science introduced its AI-powered force plate technology that predicts injury risk and prescribes personalized training programs. Another instance is Kitman Labs' Performance Intelligence Platform, which uses machine learning to analyze athlete data and provide actionable insights for coaches and trainers. In tennis, Slinger Bag launched an AI-powered ball launcher that adapts to a player's skill level and provides personalized drills. In addition, Zone7, an AI-driven injury prediction and prevention platform, has gained traction among professional sports teams recently. These innovations demonstrate how AI and machine learning have helped create new product categories and services within the sports training market, driving growth and attracting investment in this rapidly evolving sector.

Segmental Overview

The sports training market is segmented into sports type, form, application, age group, medium, component, and region. By sports type, the market is categorized into soccer, cricket, baseball, volleyball, basketball, hockey, tennis, golf, table tennis, rugby, badminton, boxing, handball, ice hockey, lacrosse, pickleball, spikeball, softball, and others. By form, it is divided into academy and coaching, therapy, and sports analytics. By application, it is classified into men, women, and kids. By age group, the market is divided into below 20, 21-35, and 35 and above. By medium, the market is bifurcated into online, and offline. By component, the market is grouped into accessories and devices, and software. By region, it is analyzed across North America (the U.S., Canada, and Mexico), Europe (France, Germany, Italy, Spain, the UK, and rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, New Zealand, and rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, UAE, Argentina, and rest of LAMEA).

By Sport Type

By sports type, the soccer segment dominated the global sports training market in 2023 and is anticipated to maintain its dominance during the forecast period. The major factors that have boosted the demand for sports training in soccer include the global popularity of the sport, the increase in youth participation, and the professionalization of training methods. The immense fan base of soccer drives young athletes to pursue the sport seriously, seeking advanced training to compete at higher levels. In addition, several sports training providers have established expertise in soccer. For instance, Coerver Coaching is well known for its player development programs that emphasize technical skills and game intelligence. Another notable provider is IMG Academy, which offers comprehensive soccer training with state-of-the-art facilities and experienced coaches. These providers represent the growing emphasis on specialized, high-quality soccer training, which thus drives the market demand of this segment.

By Form

By form, the academy/coaching segment dominated the global sports training market in 2023 and is anticipated to maintain its dominance during the forecast period. The demand for academies and coaching in the sports training market has surged primarily due to the growing recognition of the importance of early and specialized training. Parents and young athletes increasingly seek structured environments where professional coaches can offer tailored guidance, fostering skill development from a young age. In addition, the rise of sports academies offering comprehensive education and training packages has attracted those looking for holistic development, integrating academic pursuits with athletic goals. Moreover, the lack of space in cities & urban areas attracts youth toward sports academies and coaching centers. Hence, such factors propel the sports training market demand.

By Application

By application, the men's segment dominated the global sports training market in 2023 and is anticipated to maintain its dominance during the forecast period. The demand for sports training among men is primarily driven by the desire to enhance athletic performance in specific sports. Many men participate in competitive sports leagues or amateur events and seek specialized training to improve their skills and performance. These tailored training programs help athletes reach their peak performance and gain a competitive edge. Another significant factor is the increased focus on maintaining physical health and preventing injuries. Men who engage in regular sports activities often require professional guidance to avoid common sports-related injuries and to recover effectively. Moreover, programs such as those offered by Coach Logic Ltd., Skillet, and SportsEngine, among others provide structured training plans that cater to the specific needs of this segment, further fueling the demand for men sports training programs.

By Age Group

By age group, the 21-35 segment dominated the global sports training market in 2023 and is anticipated to maintain its dominance during the forecast period. Individuals in this age bracket are often highly motivated to maintain peak physical fitness and performance, driven by both personal health goals and the desire to excel in competitive or recreational sports. The demographic in between 21 to 35 age group are typically engaged in various physical activities, ranging from gym workouts and running to organized team sports, seeking structured training programs that enhance performance and endurance. In addition, engaging in sports training helps manage stress, anxiety, and depression, which are common concerns in this life stage marked by career pressures and lifestyle changes. All such factors have led to increased participation in fitness classes, boot camps, and sports leagues that offer both physical and social engagement, thus boosting the sports training market demand.

By Medium

By medium, the offline segment held the major sports training market share in 2023 and is anticipated to maintain its dominance during the forecast period. Offline sports training offers a personalized and interactive learning environment where athletes receive hands-on guidance and immediate feedback from experienced coaches. Direct interaction is crucial for skill development and technique refinement across various sports disciplines, from soccer to weightlifting, which drives the demand for offline sports training. Moreover, athletes benefit from the discipline and routine of attending scheduled sessions, which helps in achieving fitness goals and improving overall performance. In addition, the social aspect of training in groups or teams promotes teamwork and a sense of community among participants. Social interaction helps enhance the training experience and contributes to mental well-being and a supportive network for athletes.

By Component

By component, the accessories and devices segment dominated the global sports training market in 2023 and is anticipated to maintain its dominance during the forecast period. Technological advancements have significantly enhanced performance tracking through innovations in sensors, wearables, and data analytics. These technologies enable precise, data-driven training, which in turn allows athletes and coaches to rely on quantifiable metrics for optimizing performance. The rise in health consciousness has broadened the market beyond professional athletes to general fitness enthusiasts, driving the popularity of training accessories and devices. Personalization, driven by the demand for tailored training programs based on individual data, is also crucial in driving the demand for this segment. In addition, the gamification of training apps boosts user engagement, and the adoption of these technologies in professional sports influences consumer markets, which has resulted in the expansion of the accessories and devices segment in the sports training market globally.

By Region

Region-wise, North America is anticipated to dominate the global sports training market with the largest share during the forecast period. The rise in awareness of the importance of physical fitness and health has led to increased participation in sports and physical activities across all age groups. Increased prevalence of lifestyle-related diseases such as obesity and diabetes has further driven the need for regular exercise, contributing to the demand for sports training services. In addition, the professionalization of sports, coupled with the increased popularity of competitive events and leagues, has fueled the need for specialized sports training programs to enhance athletic performance.

Competitive Analysis

The key players operating in the sports training industry include Edge10 Group, Coach Logic, Firstbeat Technologies Oy, Kitman Labs, P3, LLC, Playermaker, Sparta Science, Blast motion, inc., CoachMePlus, and Shottracker inc. Several well-known and upcoming brands are vying for market dominance in the expanding sports training industry. Smaller, niche firms are more well-known for catering to consumer demands and preferences. Large conglomerates, however, control most of the market and often buy innovative start-ups to broaden their product lines.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the sports training market analysis from 2023 to 2035 to identify the prevailing sports training market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the sports training market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global sports training market trends, key players, market segments, application areas, and market growth strategies.

Sports Training Market Report Highlights

| Aspects | Details |

| Market Size By 2035 | USD 50.7 billion |

| Growth Rate | CAGR of 5.2% |

| Forecast period | 2023 - 2035 |

| Report Pages | 469 |

| By Application |

|

| By Age Group |

|

| By Medium |

|

| By Component |

|

| By Sports Type |

|

| By Form |

|

| By Region |

|

| Key Market Players | Coach Logic Ltd., Kitman Labs, ShotTracker Inc., Playermaker Ltd., Sparta Science, Firstbeat Technologies Oy, Blast Motion, Inc., CoachMePlus, P3, LLC, EDGE10 Group |

Analyst Review

This section provides the opinions of top-level CXOs in the sports training market. CXOs stated that the integration of advanced technologies such as AI, wearables, and virtual reality has completely changed the way athletes train, offering unprecedented levels of customization and real-time feedback. Technological innovation has significantly driven market expansion, as both professional and amateur athletes seek to utilize these tools to enhance their performance in recent times.

Moreover, CXOs have highlighted the importance of strategic partnerships between sports teams and training companies, which has led to innovation and expanded their market reach globally. These collaborations have benefited elite athletes and also made sophisticated training methods accessible to a broader audience. CXOs believe that the future of the sports training market will be shaped by continued advancements in technology and data analytics, which will provide deeper insights into athlete performance and recovery.

Furthermore, CXOs are expecting a surge in consumer interest in personalized training programs, driven by the growing awareness of the importance of physical fitness and the benefits of tailored training regimens. Overall, CXOs are confident that the sports training market will continue to experience robust growth, fueled by ongoing technological advancements and a rising global interest in sports and fitness.

The global sports training market was valued at $27.8 billion in 2023, and is projected to reach $50.7 billion by 2035, growing at a CAGR of 5.2% from 2024 to 2035.

The sports training market is segmented into sports type, form, application, age group, medium, component, and region. By sports type, the market is categorized into soccer, cricket, baseball, volleyball, basketball, hockey, tennis, golf, table tennis, rugby, badminton, boxing, handball, ice hockey, lacrosse, pickleball, spikeball, softball, and others. By form, it is divided into academy and coaching, therapy, and sports analytics. By application, it is classified into men, women, and kid. By age group, the market is divided into below 20, 21-35, and 35 and above. By medium, the market is bifurcated into online, and offline. By component the market is grouped into accessories and devices, and software. By region, it is analyzed across North America (the U.S., Canada, and Mexico), Europe (France, Germany, Italy, Spain, the UK, and rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, New Zealand, and rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, UAE, Argentina, and rest of LAMEA).

Asia-Pacific is the largest regional market for sports training

The key players operating in the sports training industry include Edge10 Group, Coach Logic, Firstbeat Technologies Oy, Kitman Labs, P3, LLC, Playermaker, Sparta Science, Blast motion, inc., CoachMePlus, and Shottracker inc.

The global sports training market report is available on request on the website of Allied Market Research.

Loading Table Of Content...

Loading Research Methodology...